Dire Straits (Part 2)

How a decision in London sent shock waves through global shipping

Dire Straits, Part 2

How a decision in London sent shock waves through global shipping

By Justine Isernhinke, Malone Institute Fellow and Head of Geopolitics and UAP research

It wasn’t obvious to me why Trump made this decision regarding “Security of Maritime Trade”, but after researching it, it now makes perfect sense. Another 5D chess move on his part.

The Beating Heart of London

Whilst London is known for being a financial center, what is less known is that they are the center of global insurance. Lloyd’s underwrites ~40% of the world’s marine cargo. Ship sinks, port gets bombed, canal gets blocked the bill lands in London. This is why the UK punches above its weight. Not the Royal Navy. Not diplomacy. Insurance.

Control insurance and you control trade.

85% of the world’s trade moves by sea and nearly half of it is insured through the London market.

And London doesn’t just control the global trade that moves by sea. Lloyd’s and the London market are major insurers of almost everything: skyscrapers, factories, ports, satellites - entire supply chains.

You can’t participate in public markets or raise large amounts of capital without insurance.

A small step back in history explains why.

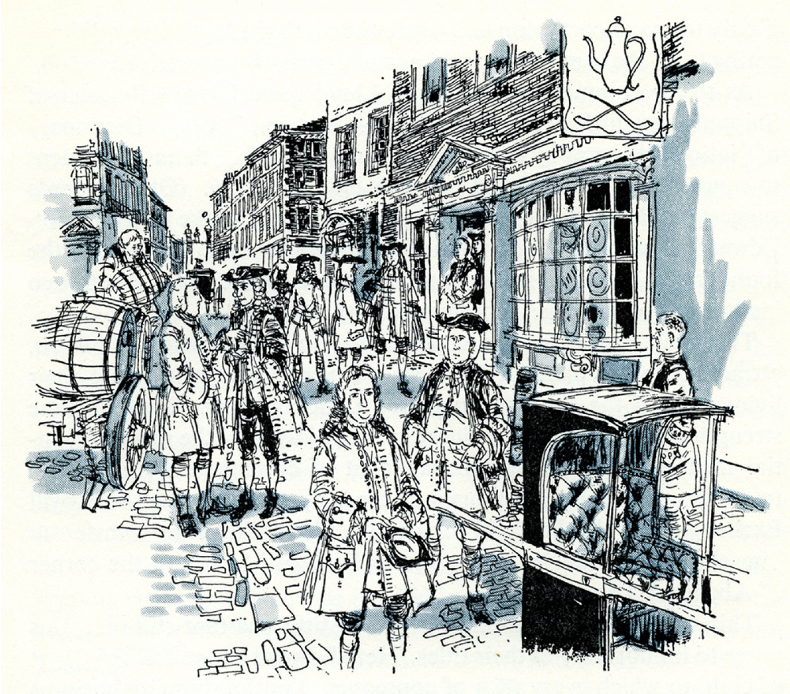

Lloyd’s Coffee House

In the 1600s, behind the busy London docks, where the air was thick with the smell of tobacco and salt, sat Edward Lloyd’s Coffee House on Lombard Street. The House attracted a buzz of merchants arguing over coffee, ship captains swapping rumors, and moneyed gamblers sizing up the odds.

It was the era where Britain found her feet (webbed feet no doubt) on the seas. The British Empire had been born. Ships, trade and colonies were beginning to boom.

By 1688, Lloyd’s evolved into the go-to spot for anyone worried about ships, storms, or pirates. If you had a vessel heading to the Americas, you could post a written proposal on the wall saying what ship, what cargo, which route, and how much money you would pay if someone agreed to cover your losses if things went wrong.

The regulars, wealthy men with an appetite for risk, would come up and literally write their names underneath the proposal, promising to pay a share if disaster struck. Hence, the word “underwriting”.

Therefore, instead of one person taking the whole gamble, several people each took a slice, spreading out the danger and the reward.

Edward Lloyd encouraged the system by renting out special boxes and private tables where deals could be struck in secret. He even installed a pulpit so he could announce the latest shipping news to the crowd. As the years rolled by, the coffee house became more than just a betting parlor.

In 1692 Edward Lloyd began selling a weekly bulletin at his coffee house with lists of ships arriving at or departing from ports, and the bulletins were also read aloud by a waiter. Details were supplied by his network of correspondents. This became the Lloyd’s News.

And then from 1734 onwards, the new owner of the coffee shop, Thomas Jemson, published the Lloyd’s List devoted to shipping intelligence, sharing news of ship arrivals, wrecks, and captures. It was a lifeline for merchants desperate to know if their fortunes were safe. That little newspaper is still running today, making it one of the oldest in the world.

What started as a smoky room full of bets and gossip quietly gave birth to the world’s first organized system for sharing risk. a system that would eventually shape the fate of almost every ship on earth.

Concentrated power in Lloyds of London

Nowadays, the doors at One Lime Street in London swing open on Monday morning, and the world’s biggest insurance marketplace wakes up. This isn’t a bank or a regular company. Inside, instead of the smokey environment of an old coffee shop, 5,000 people gather in a huge room filled with wooden desks, ringing phones, and a low hum of urgent conversation.

This is Lloyds, where nearly every ship on Earth gets insured, not by one giant firm, but by a crowd of competing teams called syndicates. There are 84 syndicates, each backed by its own investors, and each hungry for a piece of the world’s riskiest deals.

A simple vote in a glass-walled committee room of this building ripples out to every port, every warehouse, every grocery store shelf.

The price of a bowl of rice in Amman or a phone in Berlin can be traced back to a handful of experts deciding where the world’s ships are allowed to sail and at what cost.

This is how it works: Imagine you are a broker. You represent a shipowner who wants to charter a cargo vessel from Shanghai to Rotterdam. You walk into Lloyd’s with a slip, a single page summary of the ship, the route, and what it is worth.

First stop is the desk of a lead underwriter, someone with a reputation for knowing ships and storms. The lead studies the slip, decides how much risk they are willing to take, maybe 20%, and writes it right on the page. That is just the start. The broker then walks the slip around the room, syndicate to syndicate, each one deciding how big a slice they want. Some might take 10%, others just a sliver. It can take 15 or 20 signatures to cover one ship with each syndicate’s name and share written in ink. This system called the subscription model means no single group carries the whole risk. Again, think of the pizza analogy - each syndicate grabbing a piece of the pizza.

On a busy day, more than $100 million in premiums can change hands. All on the strength of these slips. The process is fast, competitive, and built for scale.

By spreading risk this way, massive fleets and rare cargos can be insured that would be too big or too daunting for any ordinary insurer. And because every deal is split among many players, the system keeps running even when disasters strike.

That is the secret behind how one building in London quietly insures so much of the world’s trade.

Solidifying Reputation

In 1906, San Francisco was destroyed by a massive earthquake and the fires that followed. More than 80% of the city was flattened, and insurance companies everywhere panicked. Most tried to wriggle out of paying, blaming the fine print or technicalities. But Cuthbert Heath, a lead underwriter from Lloyds, sent a cable to his agents in California with a simple order. Pay every claim in full, no matter what the policy said. Agents set up tables right on the ruined streets, handing out cash from suitcases.

While rival companies went bankrupt, Lloyds paid out over $1 million, an enormous sum at the time, cementing its reputation across the Atlantic.

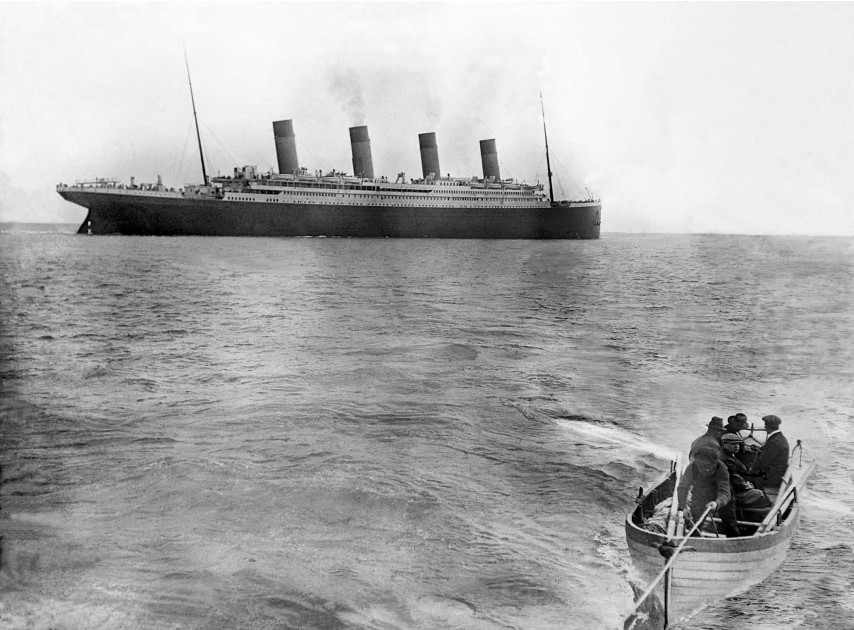

Just 6 years later, the world watched as the Titanic sank beneath the icy water. Lloyds had ensured the ship’s hull for 1 million pounds, the largest marine risk ever seen. The loss was split between nearly 50 syndicates, each taking a slice of the risk, just as they did for every ship. Within 30 days, the full claim was settled and recorded in the loss book, which still sits on display at Lloyds today.

No delays, no excuses.

Stories like these built an almost mythic trust in Lloyds. For more than three centuries, whenever disaster struck, the syndicates honored valid claims even when it hurt. That is why today nearly every major company in the world relies on this marketplace to cover their biggest risks. The system’s reputation is not just built on clever mechanics. It is built on a record of always paying up when it matters most. Cracks in the system have appeared, however.

Limitations on Lloyds

Between 1988 and 1992, Lloyds found itself facing a title wave of claims, not from shipwrecks or fires, but from old insurance policies written decades earlier, especially in America, where asbestos and pollution lawsuits piled up by the thousands.

In the middle of 1988, the Piper Alpha oil rig exploded in the North Sea, killing 167 workers and triggering a cascade of claims that rippled through the insurance market. The problem was that Lloyd’s syndicates had been reinsuring each other in tangled loops. When a disaster struck, the same loss bounced from one syndicate to another, multiplying until no one could tell where the risk truly landed. This was called the spiral.

For the wealthy individuals known as names, who had signed up to back these deals with their personal fortunes, the spiral turned into ruin. Lloyds lost nearly 8 billion pounds in just 4 years. Over 1,500 names were bankrupted. Some lost their homes, others their life savings. The pain was so deep that a few took their own lives.

Lawsuits and outrage filled the headlines. The marketplace that had built its name on trust and reliability suddenly looked fragile, even reckless. To stop the bleeding, Lloyds created a new company called Equitas. In 1996, Equitas took on the toxic old claims, giving others a a way out. 10 years later, Warren Buffett’s Berkshire Hathaway agreed to backstop Equitas with up to $7 billion. This lifeline steadied the market and allowed Lloyds to rebuild.

Today, the marketplace handles over 57 billion pounds in annual premiums and sits on more than 125 billion pounds in security. But the scars from that crisis remain. The old idea that Lloyds was too big, too historic, or too clever to fail was shattered.

Underneath the marble floors and tradition, the world’s shipping safety net is still only as strong as the people and promises behind it.

As global risks continue to rise, the world’s supply chain still relies on this fragile web of trust.

What happens if that trust isn’t enough?

The Joint War Committee

A handful of people meeting in a London boardroom can make the world’s shipping routes zigzag overnight.

The Joint War Committee (JWC) is an obscure group inside the Lloyd’s building, but with one decision, it can move trillions of dollars in global trade. The JWC

consists of senior underwriters from Lloyd’s of London syndicates) and the International Underwriting Association, which discuss key issues affecting the marine insurance market. It plays a central role in assessing and communicating heightened geopolitical and conflict-related risks to shipping. The JWC works with government personnel, security firms, and shipping companies to ascertain risk.

The JWC’s most visible and impactful role is the publishing of a list of areas - Listed Areas - of perceived enhanced risk in relation to hull war, strikes, terrorism and related perils. Ports, places, and coasts that feature on their list are assessed by an independent consultant to exceed an enhanced risk benchmark established by them. Shipowners must notify underwriters before they can traverse a Listed Area.

When the Committee adds a region to its list of high-risk waters, the effect is instant. Insurance premiums can jump from a rounding error to a budget buster in a single afternoon.

The Listed Areas are not a “ban” on insurance; the market remains open, but on much stricter, more expensive terms. Individual underwriters decide whether to provide cover and at what price (the JWC does not set premiums itself — that’s negotiated case-by-case).

In late 2023, after a wave of missile and drone attacks on cargo ships in the Red Sea, the Joint War Committee declared the area high risk. Overnight, the cost to ensure a single container ship shot up by as much as 2,700%. For some vessels, that meant paying $500,000 or more just to make one trip.

Nearly 80% of container ships decided the risk wasn’t worth it and started taking the long way around Africa. Each detour added up to 2 weeks and $1 million in extra fuel.

Suddenly, shipping companies were scrambling to recalculate everything from delivery times to the price of bananas in France.

When Russian waters were added to the high-risk list after the 2022 invasion of Ukraine, war risk premiums soared to half a $500,000 or more per voyage. Back in the era of Somali piracy, ensuring a trip through the Gulf of Aiden went from a few hundred to $150,000 with some ships hiring armed guards just to get through.

Cold Feet and the Strait of Hormuz

Shipping insurers can withdraw or cancel war-risk coverage for marine shipping primarily through contractual mechanisms built into standard marine insurance policies, particularly those covering hull (ship structure), machinery, protection and indemnity (P&I), and related war perils like strikes, terrorism, and hostilities.

These marine war risk policies (often distinct from ordinary marine insurance) include specific notice of cancellation clauses which allow insurers to terminate or restrict coverage quickly when risks surge by doing any or all of these measures:

• Short notice periods — Most policies feature a 7-day, 72-hour, or even shorter notice clause (e.g., 48-72 hours in some cargo or specific extensions). Either the insurer or insured can invoke this, but in practice, it’s the insurers (or their reinsurers) who do so when conditions deteriorate rapidly.

• Automatic triggers — Clauses often reference changes in risk, such as entry into designated high-risk zones, outbreak/escalation of hostilities, or declarations by bodies like the JWC.

• Process — Insurers issue a formal Notice of Cancellation (often via circulars or website postings) specifying the affected areas (e.g., Iranian waters, Persian/Arabian Gulf, adjacent waters including the Strait of Hormuz). Coverage continues during the notice period, then expires unless renegotiated.

Following the Joint War Committee issuing an updated Listed Areas at the beginning of March, major mutual P&I clubs such as Gard, Skuld, NorthStandard, the London P&I Club and the American Club issued notices on March 1-2 cancelling war risk insurance as of March 5 and excluding such coverage in Iranian waters, as well as the Gulf.

By expanding its Listed Areas, higher additional premiums repricing and more restrictive voyage terms and conditions for vessels entering or operating within the newly defined zones came into force. Bahrain, Djibouti, Kuwait, Oman and Qatar were added to the Hull War, Piracy, Terrorism and Related Perils Listed Areas, and the boundaries of the wider Persian/Arabian Gulf–Gulf of Oman–Indian Ocean–Gulf of Aden–Southern Red Sea region were amended.

These cancellations were caused by both by the expansion of the Listed Areas and reinsurers withdrawing support (due to unacceptable exposure). Since primary insurers rely on global reinsurers who backstop large losses, the primary insurers much follow suit or face uncovered liabilities.

The Undoing of the Five Eyes?

I read an interesting analysis of why cancellations happened when, in most cases, war risk is repriced and not cancelled. The theory goes that cancelling coverage entirely is a massive escalation in underwriting posture and signals something beyond risk - an uncertainty so deep that the underwriter can’t even price it. With Ukraine, for example, they merely jacked up premiums and made a fortune off the crisis. However, an expert in the subject whom I track on X, John Konrad, believes that London has maintained a stranglehold on global insurance because it has access to better intelligence, and that this time round, they didn’t have much intelligence.

His theory is premised partly on proximity. It’s no coincidence, he believes, that MI6’s headquarters sits directly across the Thames River from the @IMOHQ, the world’s maritime regulator, and a short distance from Lloyd’s itself. It’s long been speculated that intelligence has a direct pipeline from MI6 to Lloyd’s. Having the best intelligence in the world is the greatest competitive edge any insurer can possess, providing them with the ability to price risk that competitors can only guess at. It’s like insider trading but for global shipping

However, MI6’s intelligence doesn’t come from its own agents but from the Five Eyes alliance, which includes the US, UK, Australia, Canada, and New Zealand. And within the Five Eyes, the US’s CIA, NSA, NRO, and DIA are the dominant forces.

This leads to an interesting perspective. If the US wasn’t sharing intelligence that it was going to attack Iran - and the UK government’s reaction to the attack was one of shock and surprise - then Lloyd’s was as blindsided as the rest of London. And this means the Five Eyes is no longer the intelligence-sharing platform it once was. It was commented on several times at the start of Operation Epic Fury, that the “special relationship” between the US and UK was no longer evident.

Of course, the UK’s decision to sell Diego Garcia, home to America’s most strategically important base in the Indian Ocean, to Mauritius, was probably one of the many fissures in this special relationship.

The insurance market’s initial reaction to the war is the canary in the coalmine of this special relationship, and the future of the Five Eyes looks to be more Two Eyes - the US and Israel. Lloyd’s was pricing for being in the dark.

“What this means for UK national security is a question for the Brits. But what it means for EVERY company globally that’s insured through the London market has massive implications for the entire financial system.

Because most large insurers worldwide don’t do independent intelligence work. They index off Lloyd’s rates.

If you’re insuring a skyscraper in Tokyo, a semiconductor fab in Taiwan, or a port in Argentina you get a Lloyd’s quote, then shop that price around.

Other insurers see Lloyd’s number and assume the diligence was done. They price accordingly.

This means if London is suddenly flying blind it’s not just Lloyd’s policyholders at risk. It’s the entire global reinsurance chain.

The cancellation of war risk coverage on ships isn’t the crisis. It’s the canary.

If this hypothesis is correct, we could be looking at a systemic repricing event across global insurance markets…. the kind of cascading uncertainty that defined 2008 and COVID.

Watch Lloyd’s. Watch reinsurance spreads. What Five Eyes. That’s where this story, and possibly Wall Street, breaks.”

Repriced Risk

After issuing cancellations, the insurance companies quickly reassessed the risks, accounting for attacks, mines, seizures, loss of vessel, etc. (including lack of intelligence) and offered reinstatement or buy-back options at a significantly higher premium. Normally war risk insurance comes to about 0.25% of a vessel’s value. The premiums jumped to between 1% and 3% per transit.

• For a typical tanker valued at $200–300 million:

◦ Pre-conflict: ~$625,000 premium.

◦ Current: Up to ~$7.5 million (at 3%), or $2–3 million at 1% for VLCCs (Very Large Crude Carriers).

• For a $100 million tanker: From ~$200,000 to ~$1 million (5x increase).

This is why there is a “Closure” of the Strait without a traditional blockade. There simply is no need for a permanent physical carrier.

As Lloyd’s of London, the gold standard for maritime insurance, started cancelling policies or blowing up war risk to multiple orders of magnitude, other insurers around the world followed, some even pressured by Chinese financial interests.

It’s a quiet way to control who ships and who doesn’t. That collapsed commercial shipping traffic through Hormuz, choking off oil shipments from the Middle East.

Now it could be argued, conveniently, mind you, that this is to prevent deaths and destruction of ships. And that may well be the case. But there is good old greed here too. Insurance companies don’t like paying out insurance, as we all know. They would not want to pay out on a claim of a ship lost to war. They also realize that they literally have us between a strait and a hard place, so what a great time to make A LOT more money.

But in practice, without war-risk coverage or affordable reinstatement, vessels cannot legally or commercially transit high-risk areas, since charter-parties, financial loans, and regulations require full insurance. Without insurance, owners face personal liability for any damages or losses, leading to most shipowners opting to anchor, reroute, or halt voyages entirely.

In simple terms, if insurers won’t cover ships or the premiums are financially unfeasible, tankers stop sailing. If there is the threat of an attack, crews won’t risk their lives, and companies won’t risk billions in cargo. And once tankers stop moving, the whole system tightens up fast.

Trump’s Plan

Following President Trump’s post on March 3, 2026, the US Government stepped in the void created by Lloyd’s with offers of discounted political risk insurance.

The U.S. International Development Finance Corporation (DFC) will offer political risk insurance and guarantees to secure maritime trade through the Gulf. The initiative aims to ensure the free flow of energy and commercial trade. The DFC’s launched the $20 billion reinsurance program on March 6, 2026 for maritime reinsurance in particular including war risk coverage in the Persian Gulf region.

The DFC is the United States government’s primary development finance institution (DFI) and serves as its international investment arm. Established in 2019 under the Better Utilization of Investments Leading to Development (BUILD) Act (with bipartisan support during President Trump’s first term), DFC consolidated and expanded the functions of the former Overseas Private Investment Corporation (OPIC) and parts of USAID’s Development Credit Authority.

The maritime insurance program is designed to insure losses up to $20 billion on a rolling basis (revolving, meaning it can cover multiple incidents over time as claims are paid and capacity replenishes or is managed). It will initially apply to vessels, and serve as a backstop for private insurers to help stabilize premiums, by offering premiums at a “very reasonable” rate and minimize market disruptions amid heightened risks from the Iran war. Chubb was chosen as the lead underwriter on March 11, 2026, with a focus on hull & machinery (ship structure and equipment), Cargo insurance and war risk perils (such as attacks, seizures, mines etc.).

The plan evolved to focus on reinsurance after feedback from the insurance industry, which raised concerns about private insurers withdrawing coverage or dramatically hiking rates. It’s designed to provide support to commercial shipping charterers, shipowners, and maritime insurance companies, with the goal of reviving stalled traffic and getting oil, gasoline, LNG, jet fuel, and fertilizer flowing again.

While the Administration expressed confidence in the program’s effectiveness, some analysts have raised doubts about its feasibility, noting that the DFC’s traditional insurance caps may be insufficient for the scale of risks involved, potentially leaving gaps in coverage for damaged or destroyed vessels. No specific details on how the $20 billion is funded (e.g., from existing DFC resources or new appropriations) were outlined in the announcements.

Trump’s plan represents a government intervention to counteract the economic impacts of the conflict on global supply chains.

It’s a huge step towards reassuring allies -- both oil producers and oil consumers -- that the US’s campaign in Iran isn’t going to sink their economies. It could potentially allow the US to be choosy about traffic in the Strait. It might also mean billions of dollars in insurance premiums at wartime rates going to America rather than the UK. And those rates will still be cheaper than what shippers were getting.

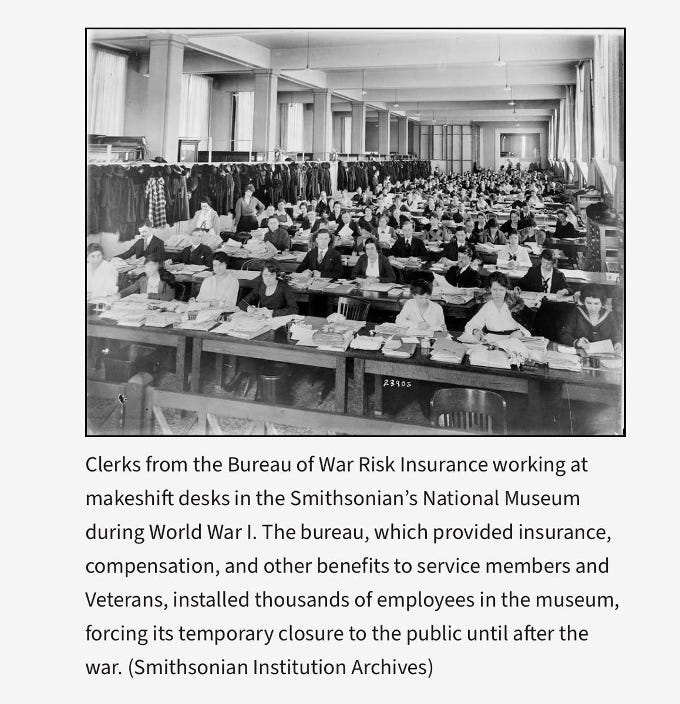

This not a new strategy, though. The US has done this historically. In 1914, Congress created the Bureau of War Risk Insurance specifically to keep American merchant ships moving during World War One. The Bureau took over the Smithsonian National Museum. During World War Two, the largest building in Manhattan was the one that managed government war-risk insurance.

In 1950, Congress expanded the authority to cover foreign-flag vessels when commercial insurance was unavailable at reasonable rates.

And then again in 1987, Reagan reflagged 11 Kuwaiti tankers under the US flag for Operation Earnest Will, which sidestepped the insurance problem entirely by bringing them under US Navy escort.

Bush activated this exact Chapter 539 authority for Black Sea trade during the 2008 Georgia crisis.

Another way to think about this is that the DFC has the chance to displace Lloyd’s as the big dog in maritime insurance game, when Lloyds has been the locked-in player. For centuries, London has been the center of gravity for marine insurance. Lloyd’s and its reinsurers control pricing, terms, and risk appetite for global shipping. That concentration is exactly what made the actuarial blockade possible. A handful of firms in one city froze global oil flows.

Then the US steps in to underwrite the risk when the private market won’t.

This unseats Lloyd’s from their dominant position. It removes the actuarial blockade and literally replaces the global marine war risk market during an active conflict. The structural implications are significant.

This move redirects billions in premium revenues to America. Ship owners get cheaper insurance.

It was also designed to send a very clear message to Iran: that they don’t get to choke off the world’s energy supply.

It shows that President Trump is thinking at the big-picture level here. Financial power on one side. Military power on the other.

Used together, they could keep the system running.

Trade and security are no longer separate conversations.

Will this solve the crisis?

On the one hand, the DFC typically provides loans to countries in the Global South. It is not in the business of marine insurance. The potential liabilities that could be incurred if the DFC/Chubb had to pay out would be enormous if there were incidents like those we saw in the Red Sea in 2023-24, with Houthi attacks on shipping.

But it does address some of the immediate premium hikes and cancellations.

It does not, however, resolve the asymmetric mosaic strategy employed by the IRGC and the Regime's toll-booth method for charging ships $2 million per passage.

To that end, how this will unfold depends on President Trump’s all-domain dominance strategy. And President Trump recognizes that the impacts of failing to address this threat are being felt worldwide.

And for that, please stay tuned for Part 3.

An important point, "the decision to sell Diego Garcia" is a misstatement. The UK, beholden to the UN and so-called international law, agreed to pay Mauritius for the privilege of giving away the Chagos Islands. Unbelievable, yes. But these socialists have a track record of making bad decisions.

Fascinating story on insurance industry leadsrship.