Dire Straits: Part 3 Ch 2

The Impact on the Global Economy - Getting to Net Zero and Lockdown 2.0

Dire Straits: Part 3 Chapter 2

The Impact on the Global Economy - Getting to Net Zero and Lockdown 2.0

By Justine Isernhinke, Fellow and Head of Geopolitics and UAP Research, The Malone Institute

The Illusion of Safety- the UAE’s bubble has burst at a cost of $120 Billion

Dubai, part of the United Arab Emirates (UAE), as an international haven, is dead right now. Expats have fled, flights are reduced, and hotels are selling rooms at rock bottom prices. Since the war started, more than $120 Billion has been wiped from market capitalization on the Dubai and Abu Dhabi stock exchanges in the last month, while over 18,400 flights have been canceled.

For reasons that remain vague, Iran targeted Dubai and the UAE from the start of the war. Two-thirds of Iran’s missiles have been launched in the direction of the Emirati nation. Dubai’s international airport was hit several times, and its world-famous Fairmont hotel on Palm Jumeirah was struck in full view of many residents. By March 28, Iran had launched 398 ballistic missiles, 1,872 drones, and 15 cruise missiles at the UAE, making it the most targeted country after its close ally Israel.

Hotel bookings collapsed, prices have been slashed, and wealthy expatriates have reportedly paid up to $250,000 for private evacuation flights.

By the end of March, Dubai’s real estate index had fallen by at least 16 percent. Goldman Sachs analysts estimate transactions have dropped 37% year-on-year, while sales have plunged by more than 50% compared with February 2026.

Some properties are now being sold at discounts of 10 to 15% by those seeking a rapid exit.

The war has also introduced “considerable risk” to Dubai’s future population growth, which now expects growth of just 1% this year and around 2% annually through 2031, well below the recent 4% trend.

An empty restaurant in Dubai

Dubai Tourism is taking a massive beating. Since almost 90% of Dubai’s population are expats, most are considering fleeing if they are able. Dubai’s economy might be one of the biggest losers in this war.

So sensitive is the fact that Dubai is no longer a safe place, that the government cracked down on anyone posting footage of the attacks.

By way retaliation, the UAE has imposed a ban on the entry and transit of Iranian nationals through Dubai.

The directive denies Iranian passport holders permission to enter or transit via Dubai International Airport. The restriction applies broadly to all Iranian citizens, including those holding valid UAE residency visas across all categories as well as holders of UAE visit and tourist visas.

The notice also says Iranian nationals currently outside the UAE, including residents, will be denied entry into the country, with the measure reflected in official application responses.

The dispute between Iran and Dubai took another surprising twist. Dubai’s exchange houses have long given the IRGC and the Iranian Quds Force access to the hard currency needed to finance Iran’s proxy groups including Hezbollah, Hamas, the Houthis and militias in Iraq. This week Dubai arrested dozens of IRGC-linked money changers, which threatens the terrorist networks that took years for Iran to build.

Air Travel taking a Nose-Dive

At the same time as Dubai and Abu Dhabi are facing an existential threat, the aviation sector, a cornerstone of the economy of the UAA, has taken a direct hit. Dubai International Airport (DXB), one of the world’s busiest airports, normally handles around 95 million passengers annually. This far outstrips London’s Heathrow which accommodates around 83 million passengers a year.

Nor is Dubai alone within the Gulf as a major hub. Rival airports in Abu Dhabi and the Qatari capital, Doha, are not quite as busy, but they still on average handle some 87 million passengers between them. Under normal circumstances, these three Gulf airports together handle more than 3,000 flights every day, the majority of them operated by the local carriers, Emirates, Etihad and Qatar Airways.

The Middle East accounts for about 5% of global international arrivals, and around 10% of US passengers traveling to Asia pass through hubs in the region.

But the conflict in the Middle East has had a dramatic impact on global aviation. At first there was the paralysis of flights through this busy airspace, leaving aircraft at other major hub airports grounded and hundreds of thousands of passengers stranded. Then, DXB suffered damage from Iranian strikes and had to shut down completely on March 1. It is back to operating but the impact is both literal and financial.

In a single day, more than 3,400 flights were cancelled across Dubai, Al Maktoum, Abu Dhabi and Sharjah. Emirates and Etihad suspended operations, with losses expected to run into the billions.

With some airspace closed, airlines including Emirates and Qatar Airways have had to reroute flights, burning more fuel. Direct Europe-Asia routes are already under pressure, with many forced through a narrow corridor over Georgia and Azerbaijan or onto longer southern paths. Longer routes and diversions lead to higher costs for air travelers.

As jet fuel prices increase, airlines will be affected depending on whether or not they hedged fuel prices, locking in rates based on prior oil prices. US carriers have little to no hedging whilst some European and Asian airlines (Singapore Airlines and Qantas) have locked in prices for part of their fuel

Air traffic in the region remains heavily disrupted. Emirates is flying roughly 70% of its pre-war schedule. Etihad has reinstated 50% of its pre-war operations. Qatar is at 20% of its pre-war schedule. Qatar sent 20 of its largest aircraft to Spain for long-term storage, to ensure their safe-keeping during the war.

According to the World Travel & Tourism Council (WTTC), the conflict is costing the tourism sector at least $600 million a day in lost international visitor spending. Before the war broke out, the WTTC had forecast that travelers would spend $207 billion in the Middle East in 2026. The blow to the travel and tourism could translate into higher flight and hotel prices — but how much higher is still unclear.

Notwithstanding the risks, Dubai International Airport has persisted with flights and remains open.

Closer to home, the CEO of United Airlines announced that the airline is operating on the assumption that oil prices could rise to $175/barrel, forcing the carrier to cut 5% of its planned capacity and remove routes. Scott Kirby is concerned that the annual fuel bill of United could rise to $11 billion which would be more than twice the profit that the airline earned in its best year.

If the Strait of Hormuz situation doesn’t get resolved in the next 2 weeks, it’s thought that at least half of all the flights in Asia will likely get cancelled over the next 2 months due to the sky-rocketing oil prices. Australia and some Southeast Asia countries will get hit the hardest. Even if an airline is willing to pay the fuel premium it will take them 40+ days to order in the jet fuel cargoes from Europe and US, as opposed vs 15-16 days from the Asian refineries in Singapore and Korea from where they usually import them. You cannot magically conjure up a jet fuel supply if the Asia refineries can’t produce them.

South Korea’s largest carrier, Korean Air, has entered emergency management mode, becoming the third Korean airline to do so following T’way Air and Asiana Airlines as jet fuel prices surge. Bankruptcies are next.

Mass cancelations of flights have begun worldwide. The Telegraph reported earlier this week that around 7% of all scheduled flights for one day were cancelled — this is more than 7,000 departures. In North America, the share of cancellations reached 14.6%.

Prices that are more than double what they were, coupled with a reduction in supplies able to transit through the Strait of Hormuz, could lead to a serious shortage of aviation fuel in less than a week.

Jet Fuel Prices in the past month:

The cost of air tickets has already risen by 15-20% in recent weeks, and demand is starting to decline.

The last known jet fuel shipment from the Middle East bound for the UK is due to dock on Thursday this week. It’s one ship. The Libyan-flagged Maetiga, loaded with jet fuel from Saudi Arabia. After that there are currently no other UK-bound cargoes from the region visible on the water.

The UK phased out Russian jet fuel supplies and replaced them with fuel routed through the Strait of Hormuz. That route is now effectively closed.

Europe sources around 40% of its jet fuel through the Hormuz chokepoint. The UK is particularly exposed, both directly and through imports routed via the Netherlands and Belgium.

Britain’s London Heathrow is the highest-risk major airport in Europe for jet fuel from April as US-Israel war on Iran continues. Heathrow, with 1,300 flights daily, will struggle ‘the most and the earliest’ with jet fuel as shortage worsens and price surges.

The impact on Food Security

The Gulf States, for whom cargo ships have all but ceased to arrive, import approximately 80-90% of their food - 70% arrives by ship through the Strait of Hormuz. The Gulf nations have strategic reserves of vital foods to cover 4-6 months of needs, which were created years ago as concerns about food supplies increased during past crises and disasters. Some perishable items like bananas can be flown in but that leads to high prices. Container prices have also leapt from $1,500 to $4,000 per container (for context, the typical cost of moving a container from Shanghai to Europe is around $2,700 – 3,600 including costs).

But hoarding, price spikes and https://www.ifpri.org/blog/the-iran-war-potential-food-security-impacts/ are inevitable unless the Strait is opened soon. We could see Gulf states subsidizing food at a time when the Gulf States will be short on cash from the halt on oil sales.

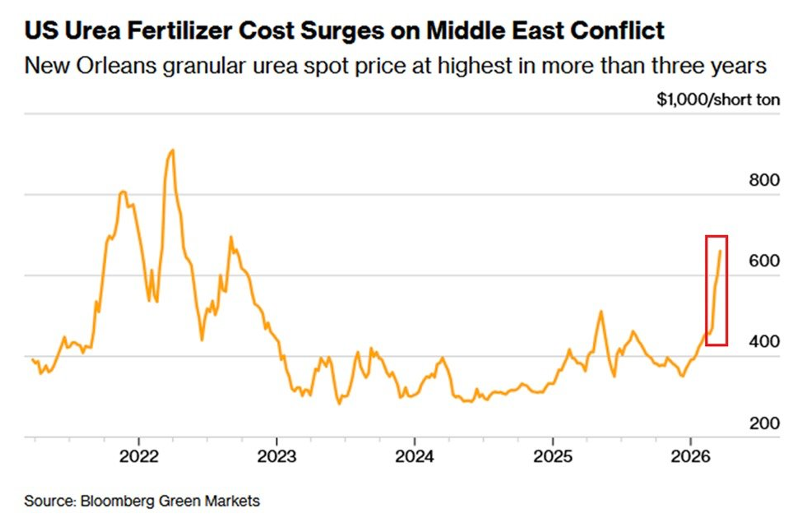

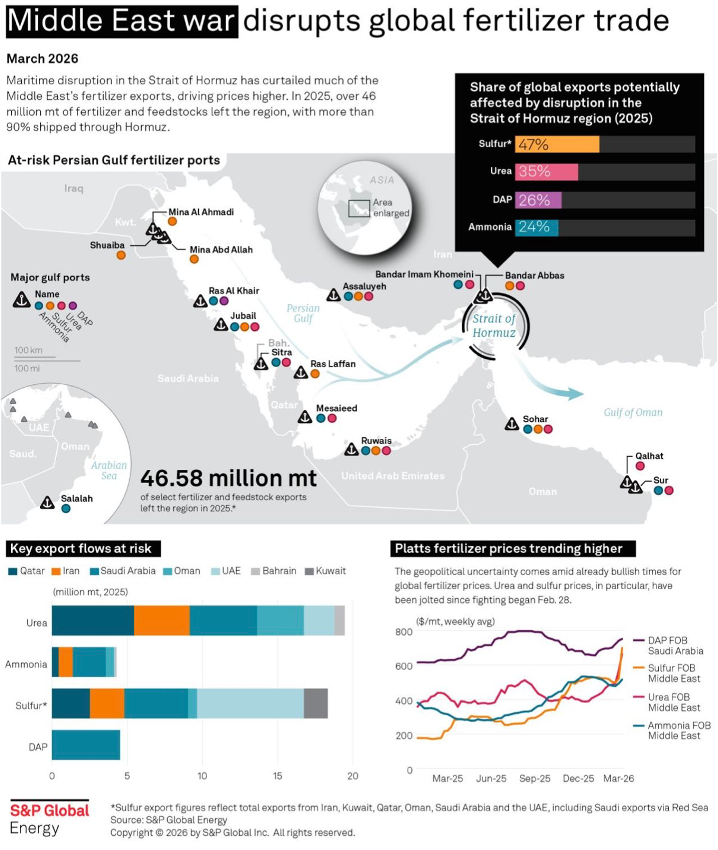

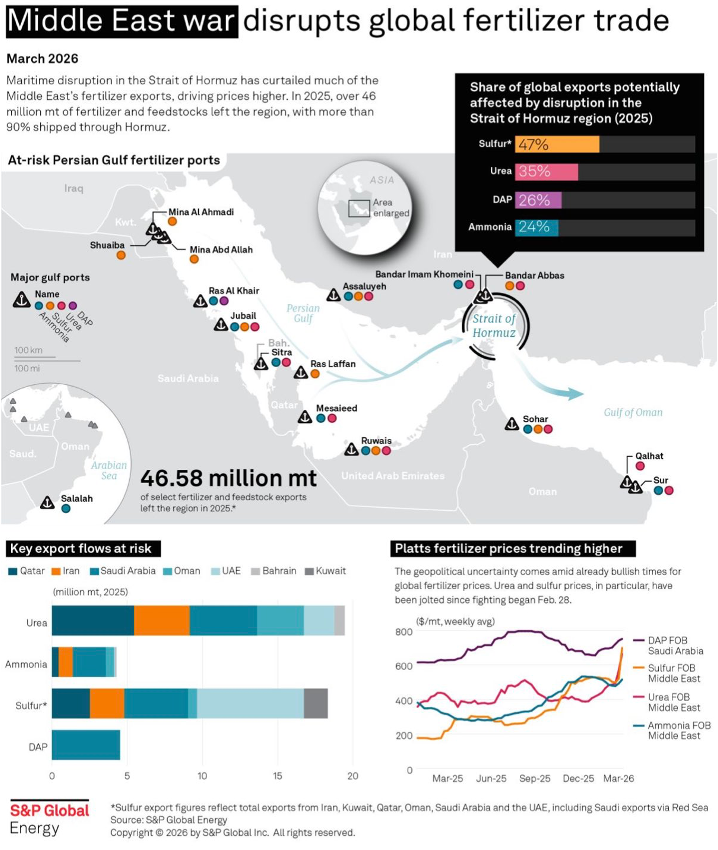

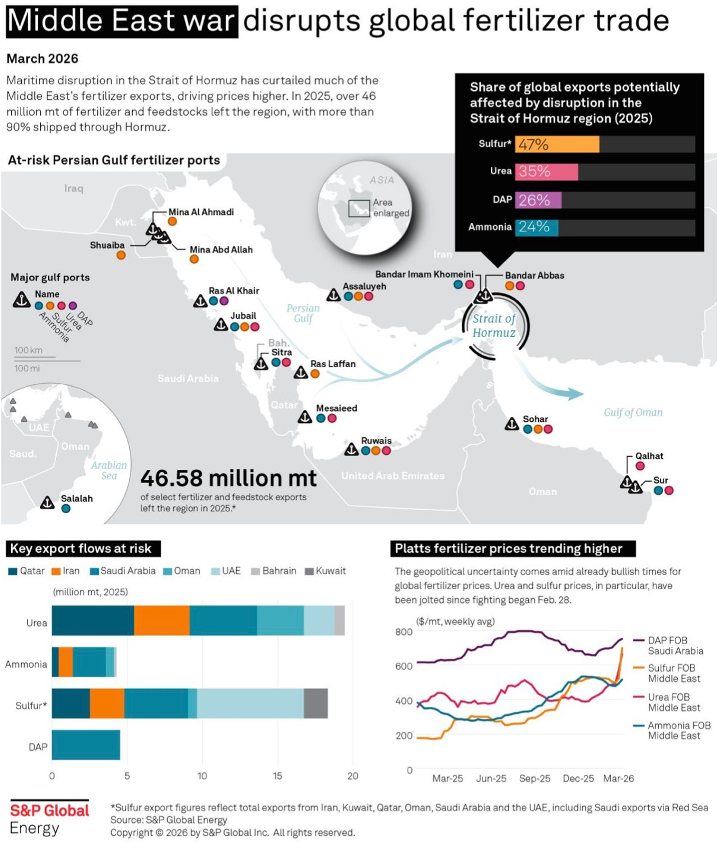

Worldwide there will be serious impacts on the food supply. Approximately 20-50% of the international trade in fertilizer exports for urea, sulphur, phosphate and ammonia ship through the Gulf.

The spring planting season has begun across the Northern Hemisphere, but farmers face soaring fertilizer prices (typically nitrogen fertilizer – also referred to as urea). The The Fertilizer Institute predicts that US farmers will be short some 2 million tons of urea this spring. The United States is currently the world’s top LNG producer, which supports a robust domestic fertilizer industry. However, the US still imports about 25% to cover the spring planting surge. About 15% of fertilizer imports to the U.S. are from the Middle East, and about half the global supply of the key ingredient urea comes from the region, along with 30% of ammonia, according to the American Farm Bureau Federation.

Fertilizers are generally applied just before or at planting, so crops miss key early growth stages and yields can fall when deliveries are delayed, even if supplies improve later. The impact is already being felt in the United States and Europe, where the main planting season is underway, and it is expected to hit the first planting season in much of Asia in the coming months. Fertilizer shortages and price hikes hit farmers hard, forcing them to use less and leading to reduced yields. Even short delays can reduce maize yields by about 4% in a season.

“We’re being told that many of our farmers that haven’t preordered their fertilizer and paid for it may not even obtain the fertilizer that they’re going to need during the season or for spring planting.That’s why this situation is so serious.”

~Zippy Duvall, President of the American Farm Bureau Federation

Many American farmers haven’t yet secured fertilizer for this year’s planting season. New Orleans granular urea prices. The most widely used nitrogen fertilizer are up 89% since December to $660 per short ton. By comparison, the 2022 peak during the Russia-Ukraine war was $910 per short ton. Top exporters China and Russia are also curbing crop nutrient sales, tightening supply further at the worst possible time, right before the spring planting season.

Meanwhile, Australia’s top fertilizer input plant had to be shut for two months to repair damage caused by a power outage. Very bad timing for Australian farmers.

Talking of food, it’s important to be aware of another significant risk in the Gulf states for those nations that depend on water desalination. Desalination plants are dotted along the shoreline of the Persian Gulf. The six Gulf states now count for some 3,401 operational desalination plants, comprising 19% of all desalination facilities worldwide. Collectively, these plants can churn out 22.67 million m3 of desalinated water each day—enough to fill over 9,000 Olympic-size swimming pools—representing 33% of global daily production capacity.

The statistics are profound and highlight just how vulnerable these countries are. Qatar derives 99% of its drinking water from its network of desalination facilities, and for Kuwait and Bahrain over 90%. For Oman, Saudi Arabia, and the UAE, the figures are 86%, 70%, and 42%, respectively. Cities such as Doha, Dubai, Manama, and Kuwait City would not be possible without desalination.

If the water in the Persian Gulf is contaminated either through oil leaks from a sinking tanker or through radiation fallout from an Iranian nuclear reactor, the contamination would be millions of lives at actual and imminent risk.

Price of Plastic

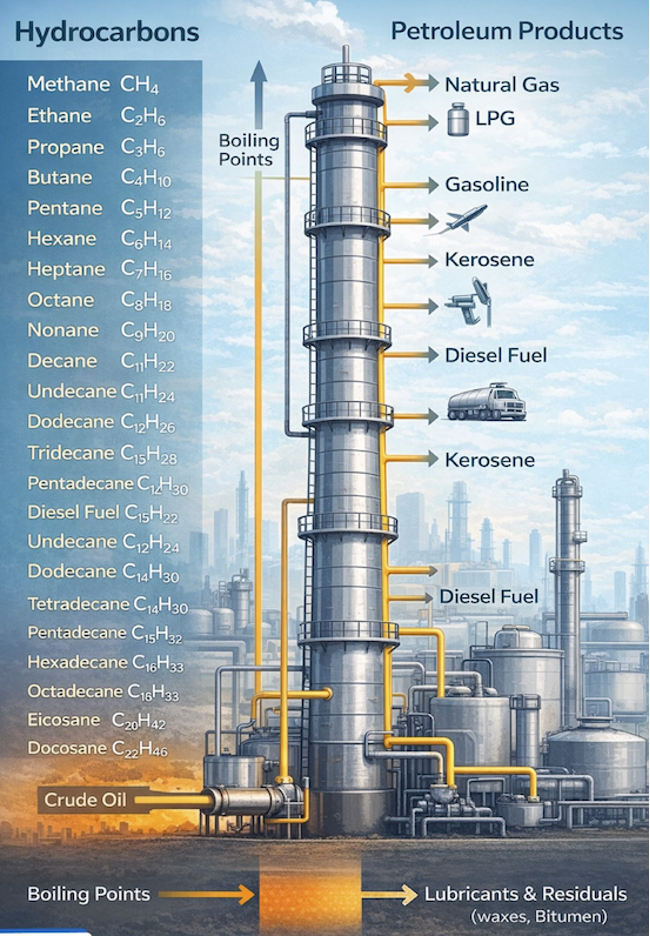

From one barrel of crude, we get these petroleum products:

@BBC

More than 99% of global plastics are derived from fossil fuels, including polyethylene (PE) and polypropylene—two of the most widely used materials.

Oil permeates our lives in so many ways, that we cannot disintermediate the substance from our lives as easily as the Climate Change movement had thought with the ban on plastic straws. It’s everywhere and in every part of our supply chain. Even if you’ve managed to purge your life of most plastic, almost all food is packed with some form of plastic. About $20 billion to $25 billion worth of petrochemical products pass through the Strait annually. The Middle East accounted for over 40% of polyethylene exports in 2025.

It’s estimated that the Strait’s closure could disrupt nearly 1.2 million barrels per day of global naphtha export flows, further tightening feedstock availability for the production of petrochemicals. This has sent Asia’s naphtha refining margin above $400 a ton over Brent crude from about $108 a ton before the conflict started. This means that higher packaging costs may drive up food prices in two to four months as companies work through existing inventory.

· Polyethylene (PE): Prices have risen sharply, with some reports indicating increases of 10 cents in March.

· Polypropylene (PP): Prices on the Dalian Commodity Exchange have risen over 38% since late February 2026.

· PVC: Prices are rising, with some additives seeing increases of up to 50%.

· General Trends: Resin prices continue to be volatile, often tracking higher crude oil and feedstock costs

Prices for plastic resins have already surged by double digits across most manufacturing categories in the past 30 days, according to the Plastics Exchange, an independent clearinghouse that tracks transaction data for the resin market.

This is likely to push up prices for products such as disposable cutlery, bottled drinks and garbage bags in the coming weeks.

Plastics are widely used across industries, from packaging to factories, making cost increases difficult to trace directly in final product prices. In the car manufacturing, the impact may take less than a year to materialize, as pricing is typically governed by longer-term contracts.

The Middle East accounts for roughly a quarter of global exports of these plastics, meaning logistical disruptions in the region have a significant impact on pricing.

Data from Plastics Exchange show that resin prices have surged by double digits over the past 30 days across multiple manufacturing sectors.

The chief execution of Plastics Exchange, Michael Greenberg has described the current monthly increase in polyethylene prices as the largest in 25 years.

Formosa Plastics has declared force majeure from April 1.

Sadara Chemical, a $20 billion joint venture between Saudi Aramco and US giant Dow Chemical, has shut down all production at its Jubail complex indefinitely, citing supply chain disruptions. Sadara is one of the world’s largest integrated petrochemical facilities, with an annual production capacity exceeding 3 million metric tonnes of chemicals and plastics. It produces ethylene, propylene, polyethylene and other key industrial chemicals used in everything from packaging to construction.

If you can stomach another Bloomberg hit, this podcast covers the impact in a less serious way:

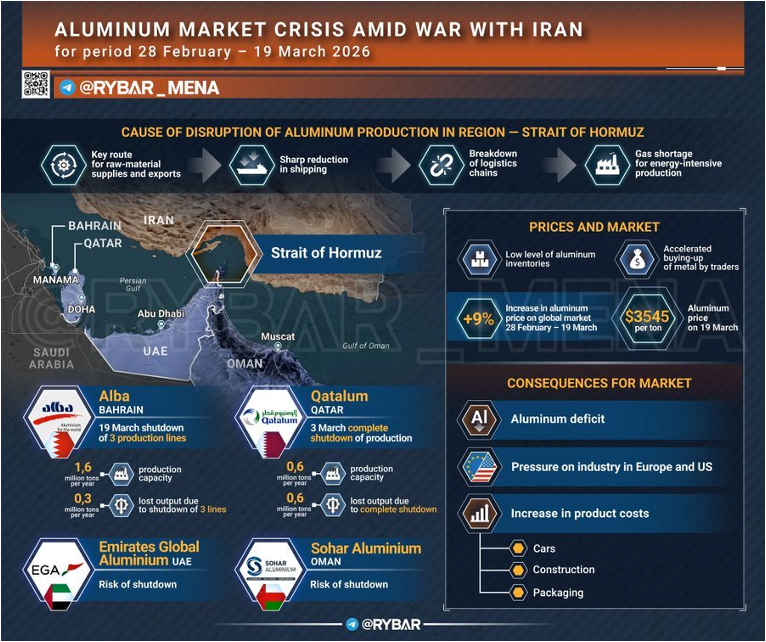

Aluminum production in the Gulf has halted as well:

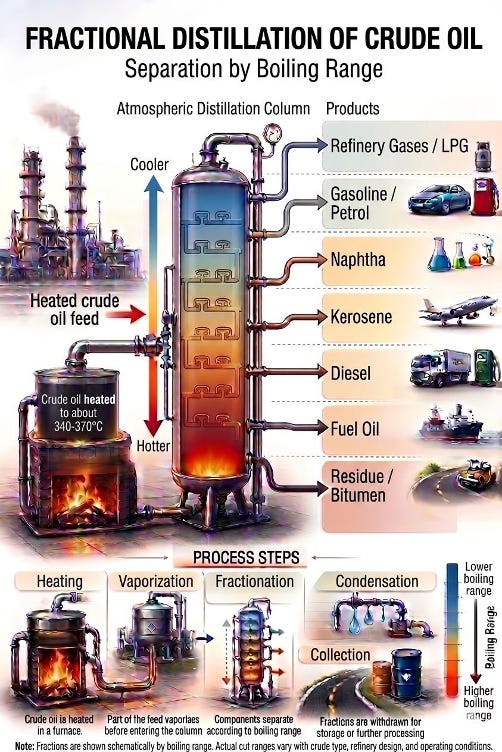

The Components of Crude

Crude oil is a mixture of hydrocarbons, from light methane (CH₄) to heavy C20+ molecules.

In a refinery distillation :

• Light molecules rise. Natural gas, LPG, gasoline.

• Mid-range chains condense in the middle. Kerosene, jet fuel, diesel.

• Heavy long chains stay lower. Lube oils, fuel oil, residuals.

The longer the carbon chain, the higher the boiling point. The higher the boiling point, the heavier the product. From C1 to C22+, the refinery separates value by physics. Temperature becomes money.

Every liter of fuel is a controlled sorting of molecules by boiling point.

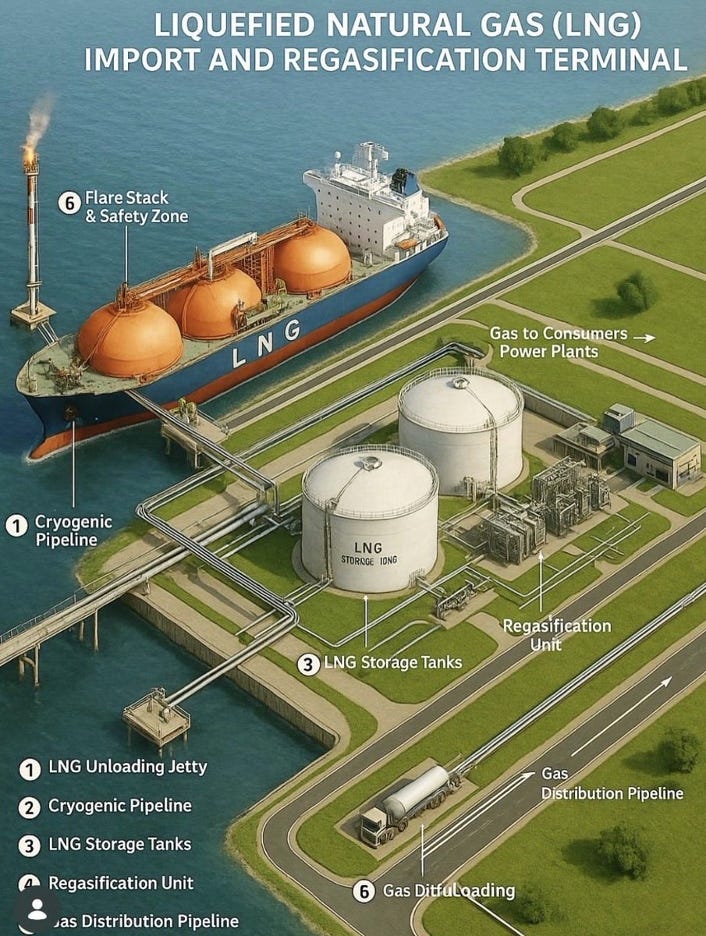

Liquefied Natural Gas (LNG)

Liquefied Natural Gas (LNG) relies on highly engineered, capital-intensive infrastructure designed to ensure security of supply, flexibility, and market optionality.

20% of the world’s LNG transits through the Strait. Similar to that of oil. Supply disruptions will be as impactful as those of oil.

An LNG import and regasification terminal typically integrates several critical components:

• Marine unloading facilities allowing LNG carriers or FSRUs (floating storage regasification unit) to safely berth and transfer cargo

• Cryogenic transfer systems operating at -162°C to move LNG from ship to shore

• Full-containment LNG storage tanks providing strategic buffer and seasonal flexibility

• Regasification units converting LNG back into gaseous form using seawater, ambient air, or closed-loop systems

High-pressure send-out pipelines connecting terminals to national gas grids, utilities, and power plants

• Safety systems including flare stacks, exclusion zones, and continuous monitoring

Beyond engineering, LNG terminals play a strategic role:

• Enable diversification away from pipeline dependency

• Support energy security during demand peaks or supply shocks

• Create trading optionality between regional gas markets

• Anchor long-term off-take, tolling, and capacity contracts

• Act as gateways between global LNG flows and domestic consumption

In today’s energy landscape, LNG infrastructure is not just physical capacity, it is geopolitical leverage, price stability, and strategic flexibility.

Taiwan – LNG and Helium

Taiwan’s grid now relies on LNG for up to 48 percent of its power generation, up from around 17 percent in 2006. Taiwan relies on imports to meet 95 percent of its energy needs in 2025, including over 99 percent of its demand for oil and natural gas.

To address the supply shortfall the war has created, Taiwan has assured the public that it has about 150 days of oil supply in reserve and has secured sufficient supplies of liquefied natural gas (LNG) to meet consumption needs through April – that being about 11 days of LNG reserves. As a comparison, South Korea stores at least 52 days of LNG and Japan holds about three weeks of stockpiles, it said.

Taiwan has attempted to mitigate the risks of its reliance on natural gas imports by diversifying LNG suppliers. Nevertheless, Qatar still accounts for around a third of the island’s LNG imports, meaning an extended Strait of Hormuz closure, production stoppage or the usual summer surge in electricity demand could create severe energy shortages if shipments through the Strait of Hormuz don’t resume soon.

Aside from energy dependence, Taiwan’s semiconductor industry depends on chemicals, components, machinery and other materials from abroad, including helium and sulfur. The conflict could choke off key supplies vital for chipmaking and spike the cost of power in Taiwan.

Any interruptions to the nation’s helium, one-third of which is processed in Qatar, sulfur, which is made through oil and gas refining would affect Taiwan Semiconductor Manufacturing Co, it said.

“A disruption in the Strait of Hormuz wouldn’t automatically halt chip production, but it could ripple through power costs, materials supply, and the economics of building AI infrastructure,” Shawn Kim, head of Asia technology research at Morgan Stanley, told Bloomberg.

Helium and MRIs

The estimated 50,000 MRI machines operating worldwide. Each one requires liquid helium cooled to minus 269 degrees Celsius to keep its superconducting magnets functional. A single non-operational MRI eliminates 20 to 30 patient scans per day. Until the conflict started Qatar’s Ras Laffan facility produced a third of the world’s supply as a byproduct of liquefied natural gas. Ras Laffan was struck by Iranian missiles on March 18. Fourteen percent of its helium capacity is permanently destroyed. Repairs will take three to five years.

Helium is also critical for AI.

Consequently, Helium prices have doubled. India’s hospitals are already reporting MRI cost spikes and scan delays. European facilities are rationing non-urgent diagnostics. Air Liquide has warned customers of unfulfilled orders. And 200 cryogenic containers holding 41,000 litres each are stranded in the Persian Gulf with 35 to 48 days before their cooling systems fail and the gas vents irreversibly into the atmosphere.

“Here is the connection that should stop every health minister, every defence secretary, and every AI executive in their tracks. The same helium that cools the MRI magnet scanning a child’s brain for a tumour in Mumbai also cools the extreme ultraviolet lithography machine printing the two-nanometre transistor in Hsinchu that powers the AI model selecting bombing targets over Isfahan. Hospitals and semiconductor fabs are now competing for the same shrinking pool of the same molecule at the same temperature. The war has created a zero-sum allocation between healing and killing, and the molecule does not care ”which one wins.”

~Shanaka Anslem Perera “The Last Molecule Standing”

Facing a significant helium shortage of ~30%, the US industrial and medical gas supplier Airgas declared a force majeure, stating they would only meet up to 50% of their normal monthly helium demand amid the Iran War and would add a surcharge of $13.50 per hundred cubic feet above the contracted price Hundreds of specialized cryogenic containers, each costing $1 million, are now stuck in the Middle East.

Damage to the Kuwait-flagged Al Salmi crude oil tanker. © Photograph: Kuwait Petroleum Corporation/Reuters

Ship-building and ship costs

Aside from astronomical insurance rates and war risk premiums, international maritime trade is vulnerable to a number of other factors that push prices higher:

· Tanker charters: For a big Suezmax-class crude carrier, the average “earnings” (a standard indirect indicator of charter costs) has more than tripled since the start of the war to over $300K/day. For LNG carriers, the measure also tripled to $90/day on a reference US to Japan route. VLCCs are in super demand. With 61 VLCCs stuck inside the Persian Gulf and 55 more waiting in various areas outside the Strait ,there are currently 116 vessels which are essentially withheld from the fleet right now, causing the upward pressure seen in rates.

· Oil shipping: Like jet fuel, the cost of shipping oil jumped - from $46 per metric tonne for shipping crude from the Gulf to China on a giant VLCC class tanker to $64 at the end of March. This assumes ships are loading, which doesn’t seem to be happening.

· Ship fuel surge: The price of bunker fuel that powers ships went from $525 per tonne on the eve of war to $936 as of March 31. Price is not the only issue. Availability is. Fuel shortages are likely if the war persists. https://www.seatrade-maritime.com/security/shipowners-fear-fuel-shortages-if-iran-war-continues

· Container costs: The cost of shipping one container has risen by 20-50%. The 4 major global shipping companies (Denmark’s Maersk Line, Switzerland’s Mediterranean Shipping Company (MSC), France’s CMA CGM and Germany’s Hapag-Lloyd) all increased rates including implementing an emergency fuel surcharge. https://www.thedailystar.net/business/economy/news/shipping-costs-spiral-iran-war-prompts-new-surcharges-4128606

I may not fully understand, but appreciate, the global domino effect of so much of the world's energy being held captive by a singular theocratic sect. It is relevant that the American continent is comparatively energy independent. That Iranian leadership intends as much harm as it can wreak upon the world in multiple forms and the USA is trying to prevent this blockade speaks volumes. I only wish Eurasian countries would find the courage to protect their energy. A global coalition would quickly end this 47 year Iranian leadership global wreaking of terror.

As with any war, we must cinch our belts and brace ourselves for what comes next. The alternative…. Being held hostage by a nuclear Iran… is unconscionable. As a nation, we have been in tough places before….massive rationing in WWII. When your ration allotments ran out, you had to alter your life around that and carry on. No more gas ration coupons….bike to work. No more butter or silk stockings…..margarine and bare legs. If chemicals are not available for farmers then crop rotations are needed to repair the soil naturally and the citizenry conserves on food supply….anyone heard of Victory Gardens? Backyard food supply you grow yourself for your family. Prices going up for airplane fuel…..cancel that European vacation. We can do what we have to and will survive this, just as we always have the past 250 years! Buck up, Americans. We didn’t make it all this way being pussies! And you spoiled young ones…you get to see what your ancestors went through long before you came along! Be a help, not a complainer.