Dire Straits, Part 3 Chapter 3

The Impact on the Global Economy - Getting to Net Zero and Lockdown 2.0

Dire Straits, Part 3 Chapter III

The Impact on the Global Economy - Getting to Net Zero and Lockdown 2.0

By Justine Isernhinke, Fellow and Head of Geopolitics and UAP Research, The Malone Institute

De-Industrialization

For the better part of the last 50 years, Europe has systematically dismantled itself both economically and culturally. Laws, regulations and mandates were adopted that were hostile to fossil fuels and nuclear energy. Strict climate and environmental standards only serve increase production costs, while reducing the competitiveness of European products for export.

Under increasing legislation, vast numbers of manufacturing companies shut down operations in Europe and established themselves in China and the U.S. to take advantage of cheaper energy and less regulatory constraint. Globalization and cheaper labor and production costs attracted European companies. Regulatory burdens had a real-life cost implication: according to the IMF, internal barriers in the EU single market are equivalent to a 45% tariff on goods and a 110% tariff on services. Robert Bryce wrote an excellent article on Europe’s Deindustrialization.

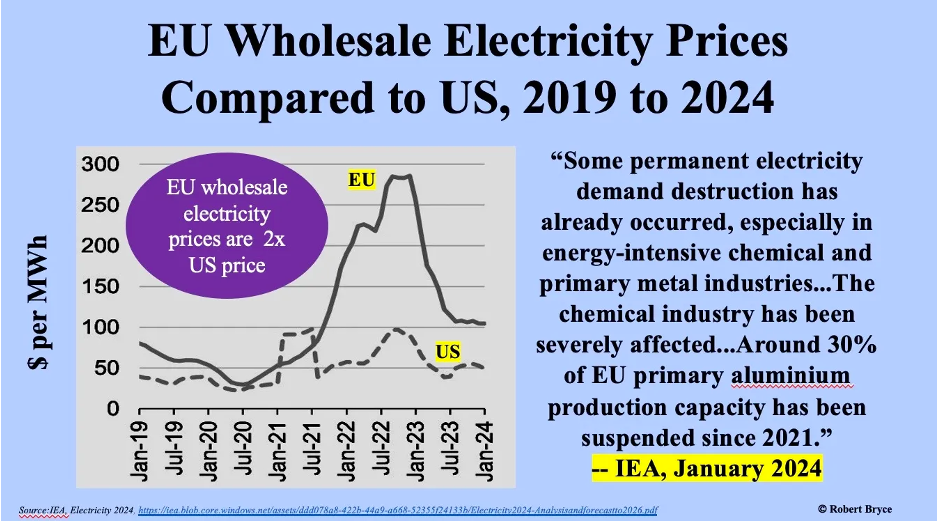

Even before Russia’s invasion of Ukraine, energy costs were higher in the EU than elsewhere. Europe’s energy crisis was made worse by the final blow resulting from the loss of cheap piped natural gas after the imposition of the West’s sanctions on Russia after the outbreak of the Ukraine war. Interestingly, Germany’s—and by extension, Europe’s—robust economic growth since the 1960s was somewhat predicated on the supply of cheap Russian natural gas supply. According to the IEA, by the end of 2024, average electricity prices for energy-intensive industrial consumers in the EU were approximately twice as high as in the US and 50% higher than in China. Not only is the European Union heavily dependent on energy imports, it is critically dependent on imports of rare earth metals and semiconductors from China and other Asian countries.

European innovation and cutting-edge technology have lagged behind the US and China for decades. There is not a single European tech giant on par with Google or Alibaba.

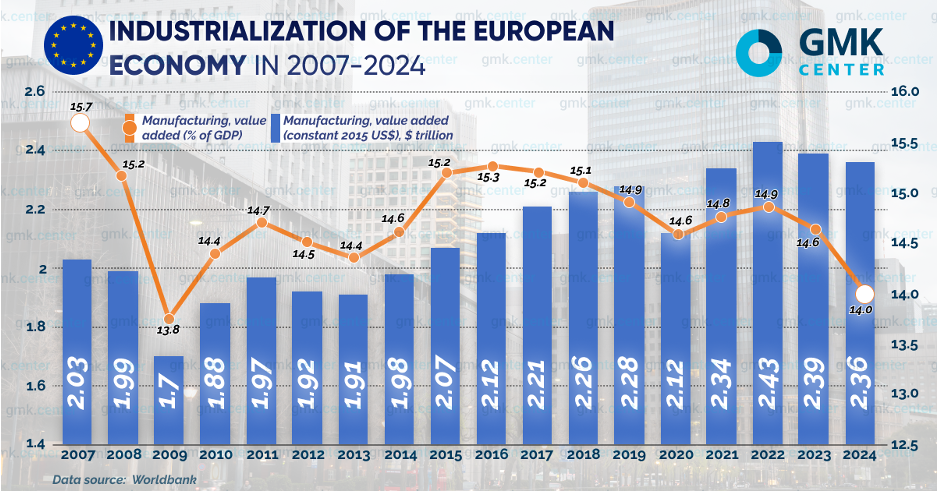

All of this has resulted in a serious and systemic industrial decline and absolutely zero capability for the continent to “take a punch” metaphorically speaking.

Gulf States Vulnerable Infrastructure

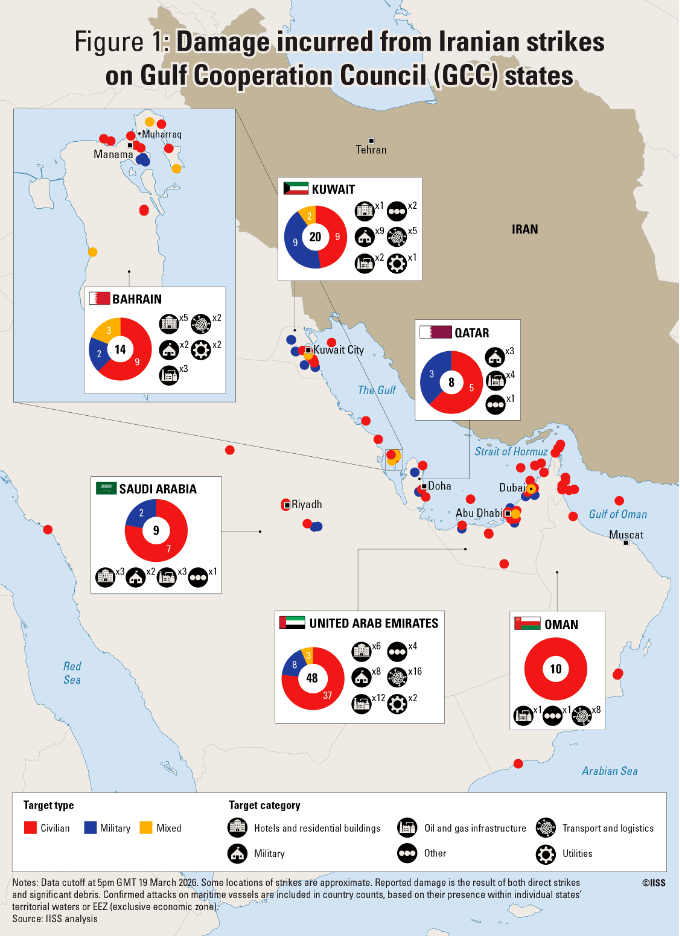

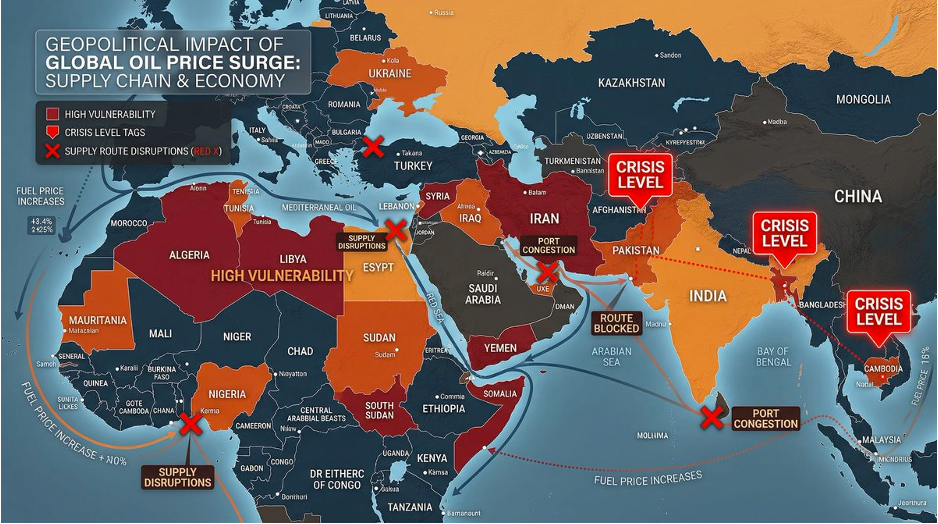

Not only have hotels and airports been targeted but the energy infrastructure in the Persian Gulf is especially exposed. As Iranian attacks have ramped up, so too have the number of successful hits on energy assets across the Gulf Cooperation Council (GCC). Key Saudi refineries in Ras Tanura and Yanbu have been hit, imperiling the pipeline alternative to the Strait of Hormuz. Iran has hit Oman’s transport and logistics infrastructure, including ports that function as partial bypass routes. Kuwaiti refineries have also been targeted: the Mina Al Ahmedi refinery came under two waves of attacks on March 19 alone.

More than 25 companies operating in the GCC, including national and international energy firms, have applied force majeure (a legal term meaning that they are unable to meet their contractual obligations and thereby waived from liability for failure to do so). QatarEnergy was the first to invoke the emergency measure after several waves of Iranian strikes on Ras Laffan, one of the world’s largest liquefied natural gas (LNG) facilities. As a consequence, QatarEnergy’s LNG-export capacity has been reduced by 17%. They estimate that it will take 3–5 years to restore the facility. Qatar supplies 20% of the world’s LNG exports, driving concerns about the security of global gas supply beyond this stage of the conflict.

As noted above, the Gulf’s premier financial center as well as a vital international shipping and transit hub, the UAE has been central to Iran’s strategy of pressuring the US by maximizing economic impact and disrupting global trade. The UAE has been attacked by more Iranian projectiles than all other GCC states combined and incurred by far the greatest and most varied damage within the group. There have been 48 confirmed hits on significant and strategic sites including Dubai’s iconic Burj Al Arab and International Financial Centre, Jebel Ali port, Fujairah’s petrochemical and storage complex, the Ruwais refinery, international airports and Amazon Web Services data centers. The concentration of these high-value targets within a relatively close geographic proximity to Iran has increased the vulnerability of the UAE’s leading economic sectors to conflict. In addition to the attacks on March 31 on the pipeline, a massive fire has broken out at a pumping station along the Habshan-Fujairah oil pipeline (ADCOP) in the UAE—a primary export route for Emirati energy products.

Iran has also sought to legitimize its disproportionate targeting of the UAE by highlighting its close relationship with Israel, with the UAE having made large-scale investments in Israeli arms and technology in recent years.

In retaliation, as mentioned previously, the UAE has literally applied extensive economic sanctions on Iran, Iranians living in the UAE, and frozen Iranian-owned accounts and seized assets.

Russia’s oil infrastructure is under attack

We will look at this more closely in the final chapter of this analysis, but Russia has obviously benefited tremendously from the increase in the oil price and the US’s easing of sanctions on the sale of oil. Simultaneously, though, Ukraine has accelerated its attacks and hit 10 major Russian refineries and export terminals, no doubt in an effort to temper any benefit Russia may have during this crisis.

Oil Prices

There are as many opinions about where the price of oil will hit as there are vessels sitting idle in the Persian Gulf. As the war progresses, and prices and shortages hit, we will also see new oil exploration, old refineries coming back online and countries doing whatever they can to secure suppliers.

David Murrin, a well-known analyst of international affairs, believes that oil will hit $350/barrel over the next few months. However, that assumes someone will be prepared to pay that price. Another analyst, Doomberg, is of the view that even if oil went to $200/barrell, there’s not enough demand for oil at that price so it won’t stay that high for that long.

We could also see a fracturing of the oil price between the West and the East.

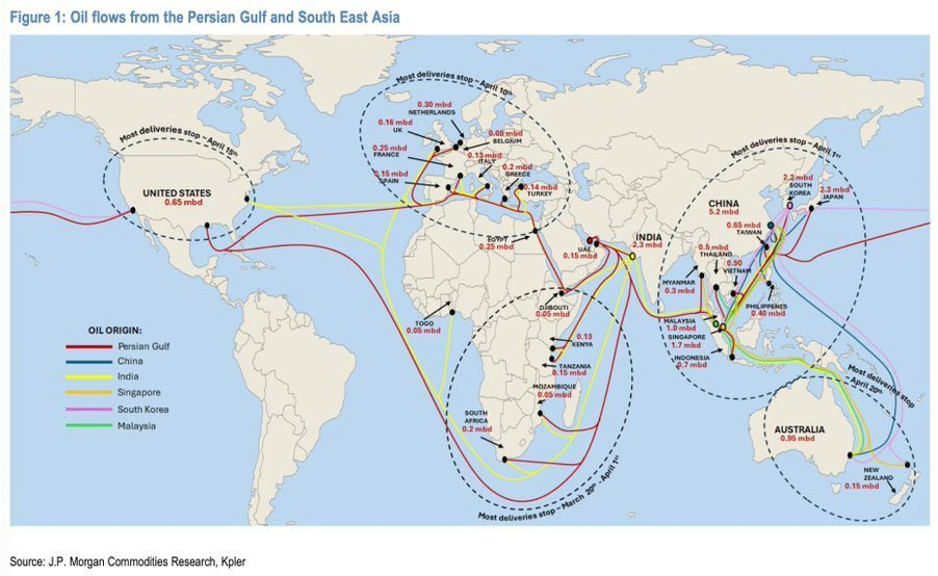

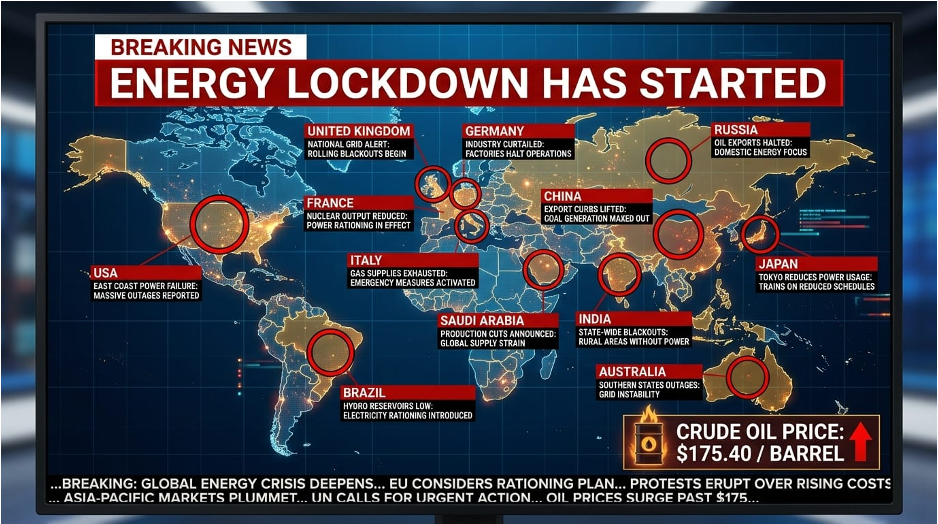

JP Morgan released a map showing how many days each continent has left before entering an ENERGY CRISIS due to fuel shortages.

Asia: April 1st

Europe: April 10

North America: April 15

Australia: April 20

For a primer on Diesel prices in the UK, check out this video:

Since Iran war began (Feb 28), here‘s what is going around the world:

CRITICAL — Running Out:

• Bangladesh — 95% imported, pumps going DRY, universities closed

• Pakistan — 80% Gulf-dependent, schools shut, 4-day workweek. Overnight price surge. Long queues.

• Sri Lanka — rationing, mandatory fuel passes, weekly holiday (4 day work week), schools closed.

• Zimbabwe — severe fuel shortages; diluting petrol with more ethanol

• Turkey - stocks crashed, inflation exploding, currency under pressure

• Australia — Tanker delays. Import dependent. Hoping IEA coordination holds.

RECORD HIGHS:

Cambodia — +68% (highest petrol hike globally)

Vietnam — +50%, panic buying, shortages

Nigeria — +35%

Laos — +33%

SEVERE — Americas:

USA — diesel +37% ($4.97/gal), gas +27% ($3.72/gal), CA: $5.29; Gas taxes suspended in states. SPR drawn down. Iran sanctions quietly paused.

Canada — +28%

Brazil — emergency fuel tax cuts; owns oil but supply chains are hurting.

Mexico — government-capped fuel prices

SEVERE — Europe:

Ireland — €2.30/L diesel (highest EU)

Germany — €2.00+/L, recession risk, industrial surcharges, gas +30%, EU emergency plan launched

France — €2.00+/L, releasing strategic reserves. Paying 30% more at pumps.

Italy — €2.00+/L, recession risk

Netherlands — €2.00+/L

Finland — €2.00+/L

Spain — +27%, €1.79/L (EU’s biggest jump)

UK — diesel +13%, inflation forecast 5%+ Shell CEO wanted of a shortage starting in April.

Austria | Portugal — cut fuel taxes

Hungary — capped fuel prices

MANAGED — Asia (but fragile):

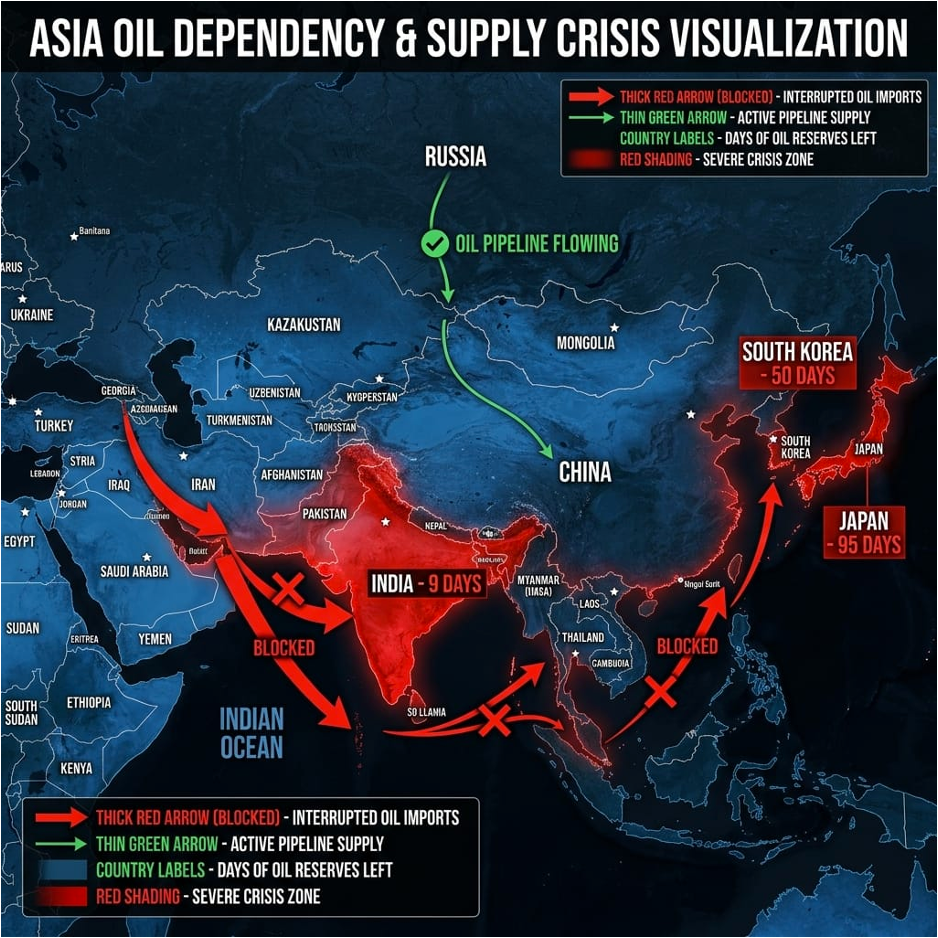

Japan — 95% Gulf-dependent, emergency reserves activated. Actual usable reserves are only 95 days. (Japan did overstate its reserves by 3x the number. Governments are desperate to keep populations calm.)

South Korea — 70% Gulf-dependent, price cap (first in 30 yrs). 50 days of reserves.

China — govt-capped +11%, banned fuel exports. 1.4 BILLION barrels stockpiled. Banned exports. Still getting Iranian oil. But China can also fall back onto other pipelines on the Asian continent.

India — only +5% (subsidized), 85% Gulf-dependent . 9 days of reserves, emergency suppliers being hunted— watch April. India’s massive textile industry has been• paralyzed with the loss of 90% of their LPG (liquefied petroleum gas) imports choked off at the Strait of Hormuz, half a million workers just lost their jobs.

Thailand — price capped. Half of Thailand’s entire fishing fleet is literally shut down because fuel prices have doubled. The global food supply chain is breaking apart because the Trump administration and Israel decided to bomb the Middle East. Philippines — state of emergency declared Mar 24; 40 days of fuel left now.

Singapore | Taiwan — Qatari LNG cut off

MIDDLE EAST / AFRICA:

Egypt — +15-22% (petrol, diesel, cooking gas — Mar 10); Egypt is reducing government fuel use by 30%

Jordan — heavy import pressure

Ethiopia — severe energy strain; prioritizing essential services for fuel supply.

Nigeria — +35%

South Africa - photos by citizens of dry gas pumps, but ANC-led government thinks the situation is “stable”

South Sudan - a 12 hour load shedding cycle because they rely on oil for electricity.

Zambia - projected welfare loss of -5.6%. The Kiel Institute warns the disruption might trigger not just an energy crisis but a food security shock due to reliance on imports.

STABLE (Producers):

Saudi Arabia | Russia | UAE

Australia out of Diesel

Australia now imports more than 90 per cent of its refined fuel, entirely on foreign-owned and foreign-crewed vessels. The war in Iran has shown how little control or influence their government has over when fuel shipments arrive, where they go, or who gets priority. Despite being a major energy exporter, Australia is uniquely vulnerable to diesel and petrol supply shocks. The deliberate closure of Australian oil refineries over a period of almost 15 years has hollowed out domestic production capacity, leaving just two facilities supplying less than 20% of the country’s needs. At the same time, Australia’s national fuel reserves fall well short of the 90-day benchmark recommended by the International Energy Agency.

Australia’s Prime Minister already is hinting at the energy lockdown that’s coming.

South Korea’s Measures

South Korea is becoming the canary in the coalmine. The Korea Composite Stock Price Index (KOSPI) has marked a fourth straight session of losses as of March 31, 2026. The Korean won has fallen to a 17 year low— levels previously broached only in the aftermath of the global financial crisis in 2009 and the late 1990s Asian crisis.

South Korea imports 70% of its crude oil and 25% of liquefied natural gas from the Middle East. The government has sought to pivot to coal as an alternative source, removing an 80% maximum operation limit, and nuclear energy by raising the nuclear power plant utilization rate from around 70% to over 80%.

The government has also imposed a five-day, license plate-based rotation system to restrict public-sector vehicle traffic and reduce oil consumption, and urged households to take shorter showers and charge phones during the day. Further - harsher - measures are being considered.

Unemployment

We have a convergence of Artificial Intelligence, a private credit crunch (banks have been limiting redemptions across credit funds for a few months now) and rising costs in all supply chains, which will negatively impact employment across the world. I listened to an interesting analysis that companies, particularly US companies, are no longer able to pass the costs onto consumers. After a year of tariffs, it’s clear to most CEOs that raising prices will price them out of the market and reduce consumption. The implications of this war, aside from any other considerations, will have a direct and unfortunately downward impact on disposable income, which was already strained with post-Covid inflation.

What can we expect?

Evergiven Ship – for every one day it blocked the Suez Canal (six days in total), there was a week of supply disruption. With the Evergiven, however, only 400 vessels were stuck waiting on the stuck cargo vessel.

Based on the logistics nightmare of Evergiven, even if the war ended today, after a month of war, we’re looking at 28 weeks of supply disruption.

Even if the war ended tomorrow, supply chains are gummed up and would take likely 6 months to rectify - at least. Recent thinking is that this could even be a year before prices come down. This could be the start of the Great Depression of the 21st Century.

Some good news

Not all is lost. If nothing, humans are incredibly adaptable and our prime directive (aside from survival) is how to make a buck with opportunity presents itself:’

Kenya: the once-forgotten Lamu Port has roared to life. Long dismissed by critics as a white elephant, it has seen a 974% surge in volume. Ultra-large vessels, too deep for Mombasa and too exposed for Gulf waters, now dock at Lamu’s 18-metre natural depth. We’re also seeing Roll-on/Roll-off (RoRo) revolution in Lamu. Manufacturers are using RoRo ships – where vehicles are driven on and off via ramps – to offload thousands of cars. These are then ferried to the Gulf on small, low-risk boats to avoid the $200,000+ war risk insurance premiums slapped on large carriers entering the Strait of Hormuz.

Ethiopia: their national carrier Ethiopian Airlines has seized the moment. With Dubai and Doha mostly paralyzed by airspace risks from Iranian missile and drone strikes, the Ethiopian capital, Addis Ababa, has become the continent’s primary air-bridge. Cargo revenue is up 14%. High-value goods, such as electronics, pharmaceuticals, perishables, are now routed through the Bole International Airport, bypassing the 40-day sea detour.

To protect this windfall, Kenya and Ethiopia have launched joint military operations along the once-languishing Lamu Port–South Sudan–Ethiopia Transport (LAPSSET) corridor. This unprecedented coordination is designed to ensure that the new “safe harbour” of Lamu remains shielded from regional spillover. And because the closure of the Strait of Hormuz marooned shipping containers, an emergency air-bridge has formed. Nairobi and Addis Ababa are now the primary transit points for consumer electronics flown from Asia to Europe, thereby bypassing the the 17,700KM sea detour.

Nigeria: the country is counting its crude. Brent prices hit $120 per barrel in March. Against a budget benchmark of $64.85, daily revenues have doubled. The government has stumbled into an unexpected multi-billion dollar fiscal cushion. The Dangote Petroleum Refinery is also cashing in. In March, it issued an export tender for 84,000 metric tonnes of jet fuel and diesel. It is no longer just a domestic project – it is replacing Persian Gulf supplies for the continent.

South Africa: The main port in South Africa, Durban, has shed its reputation for congestion. It is now clocking 28 crane moves per hour, processing thousands of ships rerouted around the Cape of Good Hope with a rare level of precision.

Morocco: Royal Air Maroc has moved swiftly. Ten new international routes –including Los Angeles and Beirut – have siphoned off transit passengers who once relied on Middle Eastern hubs. Casablanca traffic is up 12%.

Namibia: Walvis Bay in Namibia has become the first reliable refuelling station for ships emerging from the South Atlantic. Bunkering demand is up 30%.

Mozambique: the country’s $20 billion LNG project has been fast-tracked TotalEnergies resumed operations in early 2026. Over 4,000 workers are racing to meet an accelerated production date. The port in Maputo, the capital, has seen volumes grow by 16% in the weeks following the war’s outbreak. Chrome and coal exporters have abandoned northern routes in favour of the safer Indian Ocean–Cape corridor.

Mauritius: The country has leveraged its mid-ocean position into a 15% revenue increase. High-end logistics and emergency repair services are now its bread and butter.

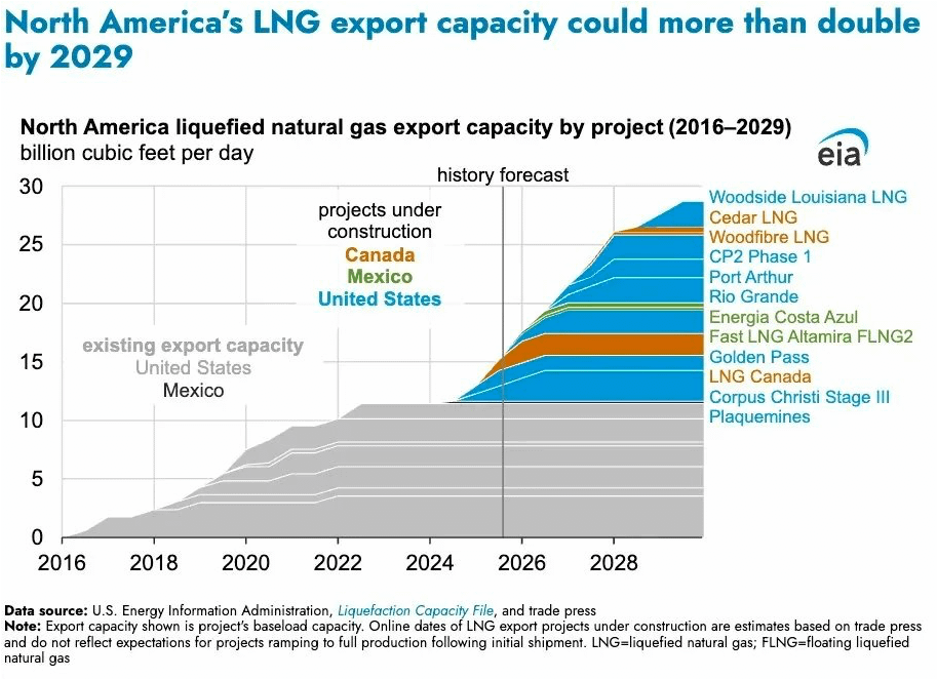

United States: The upside for the US is LNG dominance. Already the US is the world’s largest exporter at 15 billion cubic feet per day with eight new LNG terminals under construction. Capacity could double to 29 billion cubic feet per day by 2029.

We could also expect OPEC and US supply growth to have ramped up to offset Iran exports by June. By May, most Hormuz Strait volumes may have been re-routed.

There will still be a mad scramble for any oil tanker. We’ve seen China sell LNG at inflated prices to other Asian nations. A few days ago, 11 tankers carrying US diesel were abruptly diverted away from Europe towards Africa, with volumes split between West Africa and the Durban storage hub in South Africa, underscoring how quickly trade flows are being redrawn.

With passage through the Strait of Hormuz still restricted, countries are doing whatever they can to secure supply amid rising shortage risks. A similar pattern is emerging east of Suez, where cargoes originally bound for Europe from the Middle East are being redirected into Asia.

Conclusion

The European Union called for energy lockdowns and is urging Europeans to work from home, drive less, and fly less because of the Gulf conflict.. Like I’ve said, EU Energy Commissioner Dan Jørgensen says this crisis won’t end even if the war ends tomorrow. This means that Europe won’t be back to normal in a long time. Whilst there are no immediate supply shortages yet, diesel and jet fuel are already under pressure. Of course, you also have 26 of 27 EU member states currently under infringement proceedings for failing to implement electricity market rules.

The reality is that Europe’s grid is so outdated it can’t even handle the renewables they already built — 120 GW of clean energy projects are at risk of being stranded

But here’s what EU Energy Commissioner Jørgensen is not telling you:

The EU had cheap Russian energy. They chose to refuse it.

The EU had nuclear. They chose to phase it out.

Germany shut down its last nuclear plants in 2023.

Seven EU countries still actively BLOCK nuclear alternatives in energy law.

They replaced reliable energy with ideology.

Once the Gulf conflict starts to impact the EU, they have no options, no buffer and certainly no plan.

Their solution is, once again, behavioral control: tell citizens to drive less, fly less and work from home.

Then instead of telling you that the European politicians spent decades destroying Europe’s own energy production and focused on creating the most ideologically-driven, non-resilient, fragile energy grid ever, they accuse the Iran War of triggering this emergency.

This isn’t a Gulf conflict problem.

This is a European political failure dressed up as an act of God.

COVID lockdowns told you to stay home.

Energy lockdowns are telling you to stay home.

Same instruction. Different excuse.

Both times — the crisis was real. The cause was manufactured by the same class of people.

This is the most predictable energy catastrophe since the 1970s oil embargo — except this time, Europe did it to themselves.

For the last few weeks as I researched this paper, I began to wonder how we got here. What made the West so vulnerable. In fact, the world so vulnerable. I don’t know the answer to that. But there is one contributing thought I have.

When I studied economics and economic history at University, we were taught that there were progressive revolutions in humanity’s economic evolution. There was the agricultural revolution, followed by the industrial revolution, and then in the latter 20th century the services revolution. Each country had to move through each revolution in order to end up richer and more advanced. The goal was for an economy to become a “services economy” where what was produced was services and not goods or food. https://spia.princeton.edu/news/manufacturing-isnt-only-way-poor-countries-can-develop

We were taught that globalization allowed for macro division of labor – that countries that were better at producing food, should solely produce food. Countries that had cheap labor should be our factories and countries with smart intellectuals should run banks, insurance firms and technology companies – i.e. services.

What was interesting is that this development theory completely contradicted what I was taught in my international relations class about National Security.

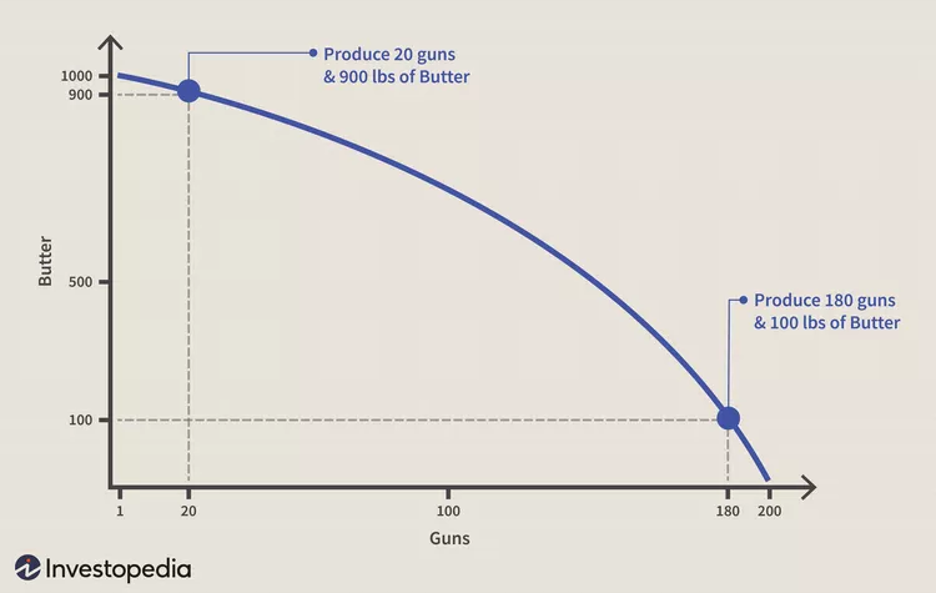

National Security is not a mythology but is rooted in the school of Realism (vs. Idealism), where the guns/butter economic debate has real world implications – do you spend money to build guns or produce butter? https://www.investopedia.com/ask/answers/08/guns-butter.asp

Under the paradigm of National Security, you really need both. It cannot be a zero-sum game. For a country to have true security, you need your own factories to churn out weapons in order to protect your people and your borders. And you need an independent food source to ensure that your people don’t starve if the countries around you stop supplying you with food.

Under National Security, the progressive revolutions of economic development are required but they never replace each other. Under Idealism, they do replace each other and economic activities we don’t like in our backyard (rare earth production, for example) need to be moved to another country that has no issue polluting its rivers and lakes.

Under the last 30 years of idealist leadership in Europe, and America to a lesser extent, we outsourced not only our call centers, but our guns, our butter, our factories, our energy production to other nations far away and out of our thoughts.

With WEF urging and EU fanaticism, Europe de-industrialized under some utopian goal of Net Zero and Carbon-Free. America was patrolling the world’s oceans, securing shipping for everyone and creating the Liberal World Order that is now eroding away as America realizes that all it did was fund Europe’s Welfare State. America was also seduced by the WEF Sirens and built up a massive service industry, to the detriment of the industrial revolution that made that service revolution possible – like coal mining, steel production, factories. However, thankfully, America is a divided nation and as idealist as some politicians were, there have been plenty of realists understanding that globalization as practiced by Europe would be the end of America. America at least has some independence – some ability to withstand what is coming.

This, I believe, is the tension we are seeing unfold on in real time today: Europe outsourced almost everything, hoping that an economy based on services would be enough to carry them through. America, especially under Trump in both terms, has held on and encouraged growth in industrialization. But I fear it’s not enough. Globalization is a fickle mistress. She has turned on those that doted the most on her.

Welcome to mandatory Net Zero and Lockdown 2.0 – all caused by politicians, economists and intellectuals who misunderstood that it always had to be guns AND butter.

The older I get the less I like war, but if I am to find obvious silver lining out of this it’s that Trump has put Americas children on notice. If you want the energy from your dealer/supplier go get it, it’s right there. It’s like cutting off your kids credit card and forcing them to get a job. Tough times create strong men. It seems Europe will face these tough times if they continue to sit on their soft bottoms and think Uncle Sucker is going to bail them out again. They will be taught a lesson or sink into a modern dark age.

In the meantime, as he did in his first term, Trump is and has been pushing American energy production, American manufacturing, and let’s not forget the Donroe Doctrine, capturing Venezuela oil. Europe and the BRICS nations have been slapped back onto their heels and are going to have to step up if they want to at all prosper. America First, if you can’t see it!

There's a lot to be said for self reliance. Most all of our ancestors lived that way. Every county in the US should set a goal of being self-sustaining, at least for food. Plant big gardens this year. Stock up the pantry. There may be hard times ahead, but Americans are resilient and resourceful. This could be a reset that provides a much needed reality check on what we think is really important in life.