The Coming Shortages

Be an Ant, not a grasshopper

By: JGM

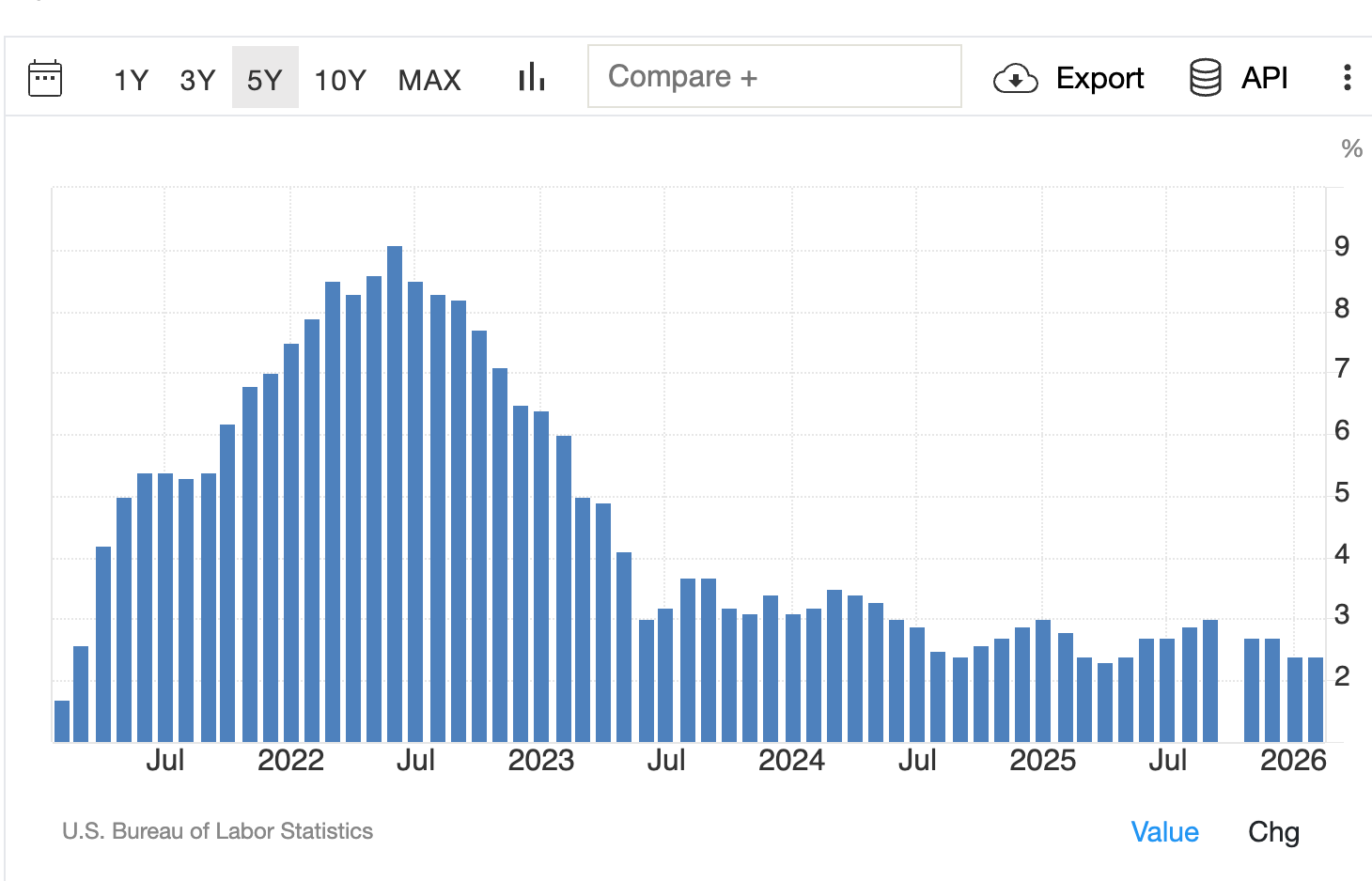

Four years ago, in 2022, I wrote a series of articles about the war in Ukraine and the eruption of the Tonga volcano, and how those events would drive inflation and shortages, causing price spikes across many categories.

That largely came to pass as I had predicted.

After Biden’s disastrous presidency, the economy under President Trump and inflation have both improved significantly.

But here we are again, on the precipice of another crisis that the media has largely missed.

First, we have the Iranian war and what it is doing to the cost of fuel. Fuel costs drive almost everything. That makes it very difficult for President Trump to use creative measures to keep inflation at bay, particularly since he does not control the Federal Reserve, which sets the key benchmarks which determine interest rates.

As the war has escalated, the situation in the Middle East has become more dire. The region has currently lost about 7 to 10 million barrels per day of effective oil production, while export flows are down more than 15 million barrels per day.

In percentage terms, that is roughly a 7 to 10 percent hit to total global supply, paired with about a 15 percent disruption to global trade flows. Add to that the Strait of Hormuz, which normally carries about 20 percent of the world’s oil, and it becomes clear that this is not just another regional conflict.

This is a large shock by any historical standard. Even small supply disruptions can move prices. A high single-digit to low double-digit disruption, combined with a logistics choke point, is enough to keep world oil prices elevated and refined product markets tight.

What matters here is that this is not just about oil that is no longer being produced. A significant portion of the problem is oil that exists but cannot move. Tanker risk, insurance constraints, and rerouting limitations mean that available barrels are effectively stranded. That is why export losses are outpacing production losses, and why the system feels tighter than the raw supply numbers alone would suggest.

Worldwide, availability becomes the bigger problem if the Strait of Hormuz remains disrupted. Oil does not get shared evenly. Higher-income countries will continue to secure supply, while more import-dependent and price-sensitive regions have begun to experience real shortages, particularly in diesel, jet fuel, and other refined products.

In the United States, the situation is different. Direct exposure to Persian Gulf imports is relatively small, on the order of 2 to 3 percent of total consumption (thank you President Trump 1.0). That means the near-term issue is not empty gas stations. It is price. Because oil is globally priced, a 7 to 10 percent global supply shock translates into higher gasoline, diesel, and transportation costs across the board.

So the immediate effect in the U.S. is inflationary pressure rather than physical scarcity. But if the disruption persists for months, those global percentages stop being abstract. They begin to show up as tightening supply chains, reduced refining flexibility, and eventually localized shortages.

Because this is a worldwide shortage, it affects inflation and supply in ways that go far beyond fuel costs. Clothing is made of synthetic materials derived from oil. Plastics come from oil. Packaging, transport, manufacturing. It all traces back.

“Soup to Nuts” is Not an Exaggeration

But here is the part that should really get people’s attention. China saw this coming early. Long before most Western governments were willing to acknowledge the scale of disruption, China began locking down key inputs. Fertilizer was at the top of that list. The CCP is not benign; when push comes to shove, it is all about China and China’s dominance in world markets. They are not honest brokers, they work to monopolize key resources and every effort should be made so that they can not do so, whether it be for semiconductor chips, lithium, or fertilizer production.

China has not shut off fertilizer exports entirely, but it has pulled back in a big way.

Depending on the product category, between 50 percent and 70 to 80 percent of export volumes are now restricted or effectively blocked. That is not a minor adjustment. That is a major contraction.

What this looks like on the ground is fairly straightforward. Key products like phosphate fertilizers and NPK blends are being heavily limited or outright curtailed.

Bottom line, China has not gone to zero. But cutting back by roughly half to three-quarters of export capacity is more than enough to cause worldwide disruptions in agriculture, particularly for countries that have come to depend on Chinese fertilizer to keep their agricultural systems running.

Fertilizer is Not Optional

Modern agriculture runs on three primary nutrients: nitrogen, phosphorus, and potassium. Nitrogen fertilizer is heavily dependent on natural gas. Potash and phosphate are mined and globally traded. China plays a major role in all three, particularly in processing and export. When they restricted fertilizer exports and prioritized domestic supply, they effectively tightened the spigot for the rest of the world overnight. A world caught flat-footed.

Now layer that on top of a war that directly disrupts two of the other major players. Russia and Belarus are among the largest exporters of potash and nitrogen fertilizers. Sanctions, shipping disruptions, and insurance constraints have all reduced availability. The Middle East, a key source of natural gas used to manufacture nitrogen fertilizers, is now unstable.

Russia has suspended exports of ammonium nitrate during the spring planting of this year, to prioritize its domestic needs:

"The restriction was introduced based on a decision of the operational headquarters of the Russian Agriculture Ministry...In the context of growing export demand for nitrogen fertilizers, suspending their supplies abroad will make it possible to prioritize meeting the needs of the domestic market during the spring field work period ," From Russia's Agriculture Ministry

This is not a small problem. This is the foundation of the global food system.

The United States is not insulated. We do produce some fertilizer domestically, but nowhere near enough to be independent, and much of the upstream supply chain remains globally entangled. Over the last few decades, we have hollowed out domestic capacity and become dependent on imports and just-in-time delivery.

Farmers operate on thin margins and tight timelines. They cannot simply wait it out. If fertilizer is too expensive or unavailable at planting, yields drop. Not a little. A lot. Corn, for example, is extremely nitrogen hungry. Cut fertilizer, and you cut yield. It really is that simple.

Farmers should be very concerned right now. But for most, the reality hasn’t sunken in yet.

And consumers will feel it, whether they realize the cause or not.

First comes the produce aisle. Fruits and vegetables, especially those that rely on intensive fertilization, will rise quickly in price. Then the staples follow. Wheat, corn, soy. These are not just foods themselves; they are inputs into everything else.

Corn becomes feed. Soy becomes feed. Feed becomes meat.

So when fertilizer prices spike, animal feed costs rise. When feed costs rise, meat, dairy, and eggs follow. It cascades through the system.

There is also a timing issue that most people miss. You do not see the full effect immediately. Fertilizer decisions made this planting season show up at harvest. That means the real impact often hits months later, and then lingers.

So what we are looking at is not just a short-term price spike, but a rolling wave.

Higher input costs. Lower yields. Tighter supply.

And ultimately, significantly higher food prices. Including restaurants.

If Oil is the Headline, Fertilizer is the Story

Energy shocks attract attention. Fertilizer shocks reshape civilizations.

This war is not just tightening fuel markets. It is tightening the inputs that grow food, move goods, and sustain modern agriculture. About a third of the global fertilizer trade now passes through the same chokepoint that is the subject of a dispute.

Energy producers, fertilizer companies, agricultural commodities, and the entire supply chain will adjust. At the same time, anything that reduces dependence on these inputs will quietly gain value.

And as always, the real story is not what is obvious today, but what shows up six months from now. Right about the same time as the US midterm elections.

One thing is clear. The United States will likely invest heavily in rebuilding fertilizer manufacturing capacity.

In the meantime, the USA is in crisis management. The administration has issued a 60-day waiver of the Jones Act to speed fertilizer deliveries inside the U.S. The Jones Act, for those who do not live and breathe maritime law, requires goods moved between U.S. ports to be carried on American-built, American-owned, American-flagged, and American-crewed ships.

In normal times, that protects domestic shipping. In times like this, it becomes a bottleneck. There simply are not enough qualifying ships to move everything, including oil and fertilizer, where it needs to go. Waiving it, even temporarily, allows foreign vessels to step in and move critical supplies along the coastline.

At the same time, the administration is seeking alternative imports from countries such as Venezuela and Morocco. But they are competing with the rest of the world for those same tons of fertilizer. That means higher prices and tighter availability are likely to persist.

Conclusion

This is not a crisis that will resolve quickly, nor one that will remain confined to the Middle East. It will work its way quietly through inputs, supply chains, and timing. First energy, then fertilizer, then food.

Most people will not notice until the cost increases reach the grocery store. By then, the decisions that drove those prices will already have been made months earlier.

So this is the window. Not for panic, but for preparation.

Tighten where you can. Plant what you can. Store what makes sense.

Because this is not just about higher prices. It is about less margin for error.

Be careful out there!

Bottom line: This is the time to tighten belts. If you have some open ground, plant a seed. The functionality of a regenerative vegetable garden makes sense for building a kitchen garden.

If you can buy a quarter cow and get it into the freezer, now is the time to pull the trigger, so to speak

As a former Phosphoric acid -Fertilizer process engineer, I am well-aware of the significance of nitrogen and ammonia in the scenario you suggest. Di ammonium phosphate (DAP) has long been the mainstay of international fertilizer market. It depend on phosphate rock (largely Russian or Moroccan), sulfuric acid (sulfur, byproduct of sour NG purification) and Ammonia. The current Haber-Bosch process for ammonia, utilizing natural gas in a steam-methane reforming operation, is expensive and wasteful.

The available of low-cost, high temperature heat from the current spate of advanced nuclear reactors will change all this. But it will take time and money. The end result will be ammonia-from-hydrogen, but the cost per ton faces a wide range of cost estimates. I, for one, am VERY optimistic, if resources are directed in the needed directions.